1-Page Summary

In Playing to Win, A.G. Lafley and Roger Martin explain their system for designing business strategies, which they developed while working together at Proctor and Gamble (P&G) between 2000 and 2015—Lafley as the CEO, and Martin as a consultant. The authors call their system the “strategic choice cascade” to illustrate how each step flows into the next. For this guide, we’ll use the term waterfall strategy instead, which is simpler and more intuitive.

They used this approach to double the company’s sales and market capitalization.

Lafley and Martin’s waterfall strategy requires company leaders to answer five questions. The questions flow into one another: Each builds on and refines the answer to the previous question while leading naturally into the next question.

The five questions are:

- What is your company’s vision and purpose, or “winning aspiration”?

- What are your target markets?

- How do you succeed in those markets?

- What capabilities does your company need in order to “win,” or achieve its purpose?

- How should you manage your company in order to achieve its purpose?

Keep Your Answers Concise

These five questions form the foundation of your waterfall strategy, but it’s important not to get bogged down in pursuing too many different answers to them. Pursuing too many options, or options that work against each other, is a common reason why many business strategies fail. Instead, make a few specific choices that, taken together, form a clear and cohesive strategy to reach your goal.

The authors say that all employees, from the CEO to a retail salesperson, have to make strategic choices. In large companies, many individual choices and broader strategies function at once and in conversation with one another. For example, one employee’s strategy could play into a brand strategy, which in turn connects with a larger sector strategy, which forms part of the overarching company strategy. Each strategy flows together to form a cohesive strategy that determines the overall success of the company—the authors call this a “nested cascade,” a waterfall made up of smaller waterfalls.

Your choices may look different depending on your position, but no matter what your job title is, the authors contend you should always play to win. In fact, this is the driving force of the waterfall strategy: You should make every choice with the express purpose of winning, not just competing. Lafley and Martin tell us competition is fierce, so if you’re not playing with a competitive mindset, you’ll be defeated by more aggressive and strategic rivals.

Counterpoint: You Can’t “Win” Business

In contrast to Lafley and Martin’s emphasis on winning, Simon Sinek argues in The Infinite Game that you can’t “win” in business. That’s because business is an infinite game, an ongoing process that nobody ever wins; the point is to play as long and as well as possible. On the other hand, games and sports are finite games—distinct events that end with winners and losers.

Sinek believes this is an important distinction because infinite games require completely different mindsets and strategies from finite games. To play an infinite game like business, Sinek recommends that you:

Focus on sustainability. Because the game lasts forever, the best strategies are the ones that you can sustain indefinitely.

Embrace flexibility. Instead of creating specific strategies to “beat” your opponents, pursue innovations and opportunities that will make your company stronger, more resilient to market shocks, or more adaptable to changing circumstances.

Take the long view. Worry more about your long-term success than your short-term profits.

In this guide, we’ll examine each step of Lafley and Martin’s waterfall strategy, then discuss how to design your own strategy to give you the best chance of dominating your chosen market. We’ll enrich—and occasionally contrast—Lafley and Martin’s ideas with advice in other popular business strategy guides such as Good Strategy/Bad Strategy, The Infinite Game, and Blue Ocean Strategy.

Question 1: What Is Your Company’s Ideal Future?

To answer the first question in Lafley and Martin’s waterfall strategy, figure out your definition of success and what you want your company to achieve. What is your “winning aspiration,” as Lafley and Martin refer to it, or the ideal future for your enterprise?

The authors say that your answer should encompass your company’s purpose, but it’s not only a statement of purpose. It’s also a statement of what success—or “winning”—would look like at your company.

The Three Perspectives of Business

A winning business strategy must address three critical elements:

The customer: Who is buying your product?

The investor: Who is covering your costs?

The producer: Who is making your product?

Many business plans fail because they only consider the perspective of the producer, the company making the product or providing the service. Such narrow business plans tend to gush about groundbreaking technologies and revolutionary ideas, but overlook the fact that they’ll need people to invest in those innovations—and, even more importantly, they’ll need people who want to buy them.

Question 2: What Are Your Target Markets?

Lafley and Martin’s second question asks: On which battlefields will your company fight, or what audience will you target? This can include fighting for customers in specific geographic markets or on particular websites, TV networks, or magazines.

Be specific about your demographic choices—figure out where you have a competitive advantage and direct your resources there.

When answering this question, Lafley and Martin suggest you consider:

- Geography: Where are you competing?

- Product: What are you offering your consumer?

- Consumers: Who are you targeting?

- Distribution: What strategy will you use to deliver to your consumers?

- Production: How much of the production of your product will you be responsible for?

- Competition: Who are your rivals in your target market? Can you offer your customers some unique value that your competitors can’t?

(Shortform note: Before starting a new business venture, entrepreneurs should ask additional questions, including, “Will this be sustainable?” When picking your playing field, it’s important to choose one that you can continue to succeed in, regardless of competition in your chosen market or costs of production, distribution, or advertising.)

Question 3: How Do You Succeed in Those Markets?

Once you’ve picked your playing field, figure out what you’ll need to win in the specific market you’ve chosen. Different companies will have different strengths: For instance, small companies can provide a more boutique service while larger companies can deliver quality products at a lower price.

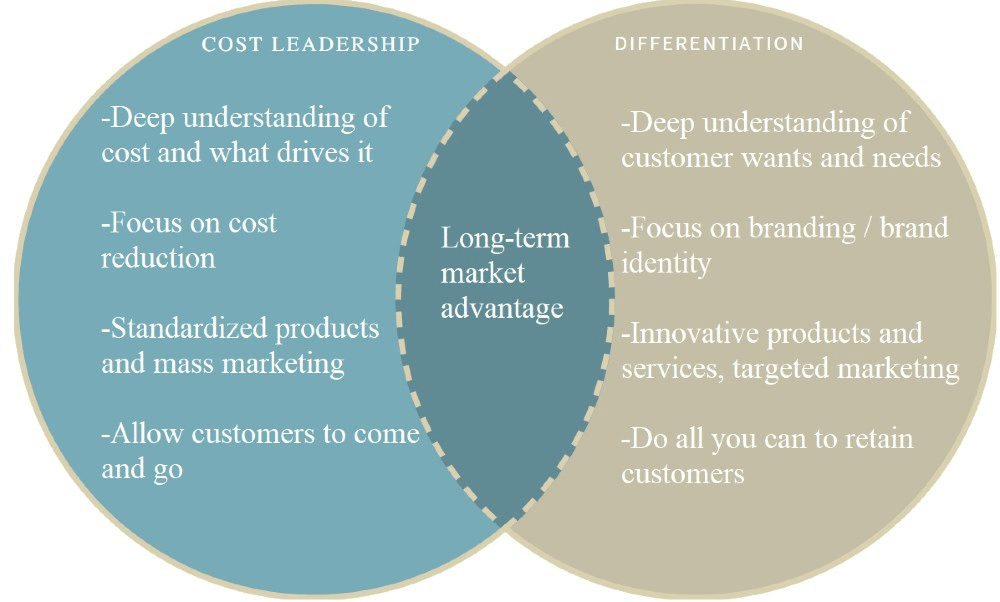

The authors identify two strategies to find victory in your chosen market: cost leadership (lower production costs and prices) and differentiation (meeting customer needs more effectively than your competitors). It’s possible to excel at both, but generally only if you’re already the dominant player in your market. Most companies have to choose one.

(Shortform note: Amazon is one example of a company that manages to be both a cost leader and a differentiator. In The Everything Store, which tells the story of Amazon from its founding in 1994 to the 2010s, journalist Brad Stone explains that Amazon founder Jeff Bezos has an “obsession” with customer service—which includes pricing the product as low as possible. The company differentiates itself by using technology and continuous innovation to meet customer needs.)

Strategy #1: Cost Leadership

In this approach, you win by selling a similar quality product at a cheaper price than your competitors. If three companies have products that are essentially the same, the authors reason that customers will generally buy the cheapest of the three. When companies cut production costs, they have more flexibility on price and are better able to undercut their competitors.

(Shortform note: Predatory pricing is an extreme form of cost leadership, in which large retailers set prices so low that smaller companies can’t possibly match them. The large retailer absorbs the losses, while smaller companies go out of business because they can’t. Once the competitors are gone, the large company raises its prices to recoup the losses and increase long-term profitability.)

Strategy #2: Differentiation

Lafley and Martin say that the alternative to having low production costs and prices is having a product that consumers want more than competitors’, because the product is either of higher quality or has better branding and prestige.

If it costs two companies the same amount to make similar products, but consumers like one more than the other, the preferred company can charge more. This leads to higher margins that companies can use to increase their advantage—for example, through higher-priced marketing campaigns or securing better retail positioning for their product.

How Brand Loyalty Works

Lafley and Martin say customer loyalty is a strong buffer against market shifts and uncertainty. Psychology professor Nigel Barber writes that brand loyalty has two main components:

Popularity: People assume that top-selling brands must be the best quality and become loyal to those brands without exploring other options.

Personality: People are attracted to brands when the advertising and presentation match their personality or how they see themselves. For example, Red Bull and Monster are two popular brands of energy drink—Red Bull advertises with silly, cartoonish commercials, while Monster presents itself as intense, athletic, and powerful. By using two different approaches, these brands capture different segments of the energy drink market.

Question 4: What Capabilities Do You Need to Succeed?

Once you’ve decided where you’re going to play and how you’re going to win, Lafley and Martin say the next step is figuring out what capabilities you need to achieve your victory, such as innovation or efficiency. To do so, determine what your company needs to be good at—and what it needs to be the best at—to win in the playing field you’ve chosen.

Note that you don’t need to outshine your competitors in every capability. For example, it’s important to be good at manufacturing, but your company doesn’t need to be the best at manufacturing to be successful (unless manufacturing is your winning strategy).

(Shortform note: While Lafley and Martin advise you to study your direct competitors, some business consultants suggest a broader view: Learn from the very best, no matter what markets they compete in. For example, if you’re trying to build up your company’s capacity for creativity, you could study companies like Google, Amazon, and Netflix—world leaders in innovation.)

Question 5: How Should You Manage Your Company?

It’s tempting to believe that if you complete the previous steps—determine your aspirations, a place to play, a way to win, and the capabilities to fulfill all of those goals—then your company will succeed. But Lafley and Martin warn that, while those steps are important, a successful company still needs three specific management capabilities to make sure the rest of the waterfall flows smoothly:

- Systems to review strategy

- Systems to communicate strategy throughout the organization

- A system to measure progress toward your goals

(Shortform note: With the coronavirus pandemic, and the resulting increase in teleworking, these management capabilities are more important than ever. Managing a work-from-home or hybrid team presents unique challenges that companies must be prepared to meet. Specifically, fairness and communication are the keys to effectively managing such a team. A clear system for measuring progress and performance ensures fairness by holding everyone to the same standards, regardless of where they work from. Clear communication ensures that your at-home employees aren’t left out of the loop.)

Capability #1: Systems to Review Strategy

Lafley and Martin say that a healthy work environment—one with good communication and happy employees—is necessary for strategic success. To foster this collaboration and deftly respond to new challenges, managers and executives must discuss issues and review strategy in the open.

According to Lafley and Martin, the best way to do this is to have regular open discussions. Focus on simple strategic questions during these discussions, and don’t expect to come up with a perfect plan in one fell swoop—strategy is a continuous process of innovation, discovery, and review.

(Shortform note: Open discussions of this nature require trust: Each person in the discussion must trust the overall company strategy, and also trust his or her coworkers to be respectful and honest. According to Simon Sinek’s book Start With Why, trust isn’t a rational feeling and isn’t tied to actions; rather, it’s tied to values. Therefore, to make these open discussions productive, first build trust by demonstrating to your employees that you share their values and their concerns.)

Capability #2: Systems to Communicate Strategy

Lafley and Martin emphasize that company leaders must communicate the organizational strategy to everyone—from senior managers to low-level employees.

First, executives need to make the message compelling by distilling the few elements of the strategy that are key to enabling the company to achieve its goals. Second, leaders must communicate the strategy in clear, simple language, which helps employees remember and carry out the strategy.

(Shortform note: When a company strategy is unclear or doesn’t resonate with employees, they don’t do their part to execute it, rendering the strategy virtually useless.)

Capability #3: A System to Measure Progress

When you create a strategy, Lafley and Martin recommend you establish expected outcomes and a way to measure results against those outcomes. Measure your company’s performance and use that data to determine what’s working, what isn’t, and how you can improve your strategy.

Lafley and Martin warn that you should never use a single outcome to determine your success. Establish individual goals for each department so your company’s overarching strategies are well-rounded, and to ensure that one missed goal doesn’t derail your motivation or morale.

(Shortform note: When setting goals, make sure that they’re appropriate for each individual department or employee, not just a “company standard.” For example, an innovative new unit within your company shouldn’t be held to the same standards as a long-established and optimized core business unit; doing so just sets that new unit up for disappointment and failure.)

Navigating the Waterfall

Now that we’ve covered the five steps of Lafley and Martin’s waterfall strategy, we’ll delve into exactly how to make decisions at each step. There’s no surefire formula for victory, but there are frameworks that, if used correctly, can serve as jumping-off points and make success more likely.

(Shortform note: Lafley and Martin say that there’s no sure way to win in the marketplace because there are always unknown variables and uncertainty in any strategy. In Antifragile, statistician and risk analyst Nassim Nicholas Taleb explains how to make uncertainty work in your favor instead of against you. One of Taleb’s key points is to always leave yourself as many options as possible; every option you have available helps you maximize opportunities and minimize harm from any sudden changes.)

Decision-Making at Early Waterfall Steps

While you work through Lafley and Martin’s waterfall strategy, remember that no decision is final. Each step of the waterfall affects all the others (not just those below it), and every strategy can change based on changing market conditions. Therefore, you’ll most likely come back to the early steps and rethink the decisions you make.

Remove Ego From Your Decisions

When responding to changing circumstances, one unforeseen obstacle can be your own sense of pride. In Ego Is the Enemy, Ryan Holiday explains that pride (or ego) can prevent us from recognizing when we’ve made a bad decision and keep us from admitting that we need to change our approach.

He explains that someone with too much ego sees failure as a personal attack, rather than simply a part of life; they become defensive, blame others, and stop working to improve the situation. This kind of emotional reaction can turn a temporary setback into a permanent defeat.

Step 1: Lay the Groundwork for a Choice

Lafley and Martin say you should begin by identifying the problem you’re trying to solve and boiling your options down to a clear either/or choice—for example, if you need to reduce overhead, perhaps your options are to either fire employees or remove yourself from a geographic area where distribution is expensive.

Next, ask what information you would need to figure out which of those solutions is best. Note that you’re not making a decision yet; your final choice might not be either of the options you just came up with. Right now you’re figuring out what groundwork you’ll need to do before making a decision.

Consider Options Using the “Toggle” Technique

As an alternative, use the Toggle Technique to consider different options. Here’s how it works:

Center yourself. Take a moment to close your eyes and breathe. You’re about to engage in a fairly strenuous mental exercise, so make sure you’re calm and prepared for it.

“Pick” an option. Think about the first option on your list and imagine that you’ve already chosen it—imagine that you’re 100% committed and there’s no going back. Does it make you feel excited? Nervous? Sick to your stomach? Your emotional responses will be the key to making this decision.

Toggle. Once you’ve examined your emotional response to the first option, switch to the next one on your list and imagine that you’re 100% committed to it. Again, check in with your feelings. Repeat this process for every option you’re considering.

Choose. Once you’ve checked in with your “gut” on every option, pick the one that feels the best.

Step 2: Imagine Potential Strategies

Now that you have two viable options, think about every possible strategy for solving the problem, no matter how off-the-wall it seems. Lafley and Martin suggest that, during these sessions, you don’t put the ideas through any sort of vetting process—just let solutions fly and imagine the positive outcomes of each. Write down every new idea, no matter how unusual.

(Shortform note: In Purple Cow, Seth Godin suggests that you use these brainstorming sessions to intentionally come up with the most extreme, over-the-top options you can imagine. Godin reasons that to create an exceptional product, you should start by finding the outer limits of possibility. Then determine which of those extreme options will get you the results you want, and figure out how to implement it.)

Step 3: Determine the Conditions for Success

After you’ve written down all of your potential solutions from Step 2, move on to figuring out what market conditions would be necessary for one of these possibilities to succeed. This requires a sort of reverse engineering—start with the assumption that each potential solution is a good one and work backward to determine what conditions would make that so.

(Shortform note: In Purple Cow, Godin explains that digital cameras were able to compete with—and eventually dominate—the photography market because manufacturers identified and then created two conditions for success: Digital cameras had to be at least as easy to use as film cameras, and people needed to understand the advantages that digital cameras had—such as not needing to get film developed.)

Step 4: Find Potential Barriers

Lafley and Martin’s fourth step is the opposite of Step 3—Figure out every potential problem with each strategy. Encourage the members of the team who are most skeptical about each idea to explain their skepticism. Do this for each of your potential solutions.

(Shortform note: Sometimes, the most successful people are those who manage to turn problems into opportunities. For example, boxing great Muhammad Ali won the famous Rumble in the Jungle match against George Foreman with the rope-a-dope: leaning against the ropes to absorb the shock of his opponents’ strikes. Foreman exhausted himself throwing powerful yet ineffective punches, then Ali struck back for an easy knockout. In other words, Foreman’s strength was a barrier that Ali couldn’t overcome, so instead he used a clever strategy to turn that barrier into an advantage.)

Step 5: Create Tests

Next, Lafley and Martin suggest you design tests—approved by the group—that can gauge both the potential success conditions and the potential barriers to each strategy. These can be qualitative (like speaking to customers in a focus group) or quantitative (like conducting large-scale price-point tests). If your company can’t afford these sorts of tests, Lafley and Martin recommend using publicly available data instead.

(Shortform note: Formalized testing isn’t always feasible. Generally, formal testing is appropriate for implementing a strategy but not for creating a strategy. For example, you can test a new company logo in a focus group. However, if you’re facing a major strategic decision like a merger, there’s no way to run a meaningful test—you’ll have to make the best decision possible based on the information you already have.)

Step 6: Administer Tests

After you’ve designed your tests, conduct them. Lafley and Martin suggest prioritizing tests based on which ideas are more and less likely to be successful. First, test the ideas about which you feel the least confident. If these possibilities fail, eliminate them right away, and move on to testing ideas that you think have a better chance of success.

(Shortform note: You may be tempted to set tests that you believe your ideas will pass, to prove that they can pass the tests. However, it’s often more effective to do what philosopher Karl Popper calls negative verification: Design tests that you think the strategy will fail to find the flaws in it. Negative verification allows you to quickly and efficiently weed out the ideas that won’t work.)

Step 7: Make Your Choice

The final step of Lafley and Martin’s process is to choose a strategy. If you’ve done the first six steps correctly, you should feel confident that the data from your tests are pointing you in the right direction. Whatever potential solution tests best is the one you should choose.

Step 8: Stick to It—Unless…

Lafley and Martin’s decision-making process is designed to help you make the best decision possible and feel confident in it, but it doesn’t include guidance for what to do when you don’t make the best decision. To avoid executing a poor choice after making a decision, set specific red flags that would get you to reconsider that decision.

Setting specific guidelines like this will help in two ways:

You won’t panic at the first sign of trouble and make an unnecessary course correction.

You won’t wait too long to make a necessary course correction.

Setting these red flags will keep you on track—you’ll be able to make changes when needed, and only when needed.

Shortform Introduction

Playing to Win is a collaboration between A.G. Lafley and Roger Martin, who worked together at Procter & Gamble (P&G) as CEO and strategic adviser, respectively. The book teaches what business strategy is and how to use it effectively. Lafley and Martin suggest using a “waterfall” sequence of five questions that identify the company’s vision, target markets, and plan to dominate those markets. The answer to each question informs the next, hence the term waterfall strategy.

About the Authors

Lafley is best known for leading P&G as president, CEO, and chairman of the board from 2000 to 2010 and from 2013 to 2015. During those periods, he doubled P&G’s total sales and market capitalization—his success is credited to his heavy investments into brands that were already successful and his intense focus on customer satisfaction. Lafley stepped down as CEO in 2015 to become executive chairman of P&G, and he officially retired in 2016. When he stepped down for the second time, Fortune hailed him as “one of the most lauded CEOs in history.”

Martin is an author, strategic adviser, and former dean of the Martin Prosperity Institute at the University of Toronto. In addition to advising CEOs of several major corporations, including P&G, Martin is known for his contributions to the theories of democratic capitalism and Integrative Thinking. Thinkers50 named Martin the world’s #1 management thinker in 2017 and regularly places him in the top 10.

Connect with AG Lafley:

Connect with Roger Martin:

The Book’s Publication

Playing to Win was published in 2013 by the Harvard Business Review Press. It was Lafley’s second book, following The Game-Changer, and, to date, it’s the last book he’s authored.

Martin (a professional author) has many more books to his name, but Playing to Win remains one of his most popular and successful.

The Book’s Context

Historical Context

A large part of Playing to Win’s appeal is that it provides a clear and easy-to-follow guide to creating a winning strategy. This was especially relevant in 2013 because the 2010s were—as the authors say in the book’s conclusion—a time of extreme globalization, thanks in large part to technological advancements and the internet. Since publication, the global marketplace has become even more complex, and it shifts quickly and constantly. That’s why it’s more important than ever for a business to have a clear and effective strategy guiding it through rapid market changes.

Intellectual Context

Playing to Win is most notable for pushing back against business guides that discuss how to compete in the marketplace. Instead, Lafley and Martin insist that the purpose of business strategy is to dominate the marketplace—in other words, to win. That, plus the authors’ focus on clear and actionable advice, helps this book stand out among the plethora of popular business guides from the 2010s, such as Blue Ocean Strategy and Tools of Titans.

Simon Sinek’s 2018 book The Infinite Game would later dispute some of Lafley and Martin’s ideas, particularly the concept that you can “win” at business. We’ve included some commentary to explore Sinek’s perspective.

The Book’s Strengths and Weaknesses

Critical Reception

Playing to Win is a Wall Street Journal and Washington Post bestseller, and it has received largely positive reviews from critics. The Financial Times calls Playing to Win a manual for business strategy. Fortune lauds the book for its insightfulness and accessibility. Overall, fans of the book believe that it’s one of the most practical and easy-to-understand business strategy guides on the market.

Criticisms of Playing to Win are generally mild, such as Fortune noting that the book’s case studies all come from large corporations like P&G or Apple, and therefore might not be applicable to smaller companies and startups. The Financial Times says that it makes for dry reading, but that the lessons it contains are worth learning nonetheless.

More serious critiques—mostly from individual reviewers on Amazon and Goodreads—take aim at how heavily Playing to Win focuses on Lafley’s time at P&G. They argue that the lessons are outdated, and that the examples and case studies are self-promotional fluff. However, the authors say in their introduction that they’ve seen their methods used to great effect in companies of all sizes across many different industries.

Commentary on the Book’s Approach

Playing to Win starts by presenting the five questions of Lafley and Martin’s waterfall strategy. The subsequent chapters explain each question in detail, including how to come up with effective answers and implement those ideas in your own business. It’s a logical structure that takes you step-by-step through the authors’ process of developing strategies.

Playing to Win relies heavily on examples and anecdotes from Lafley and Martin’s time at Procter & Gamble, which illustrate (but lengthen) their lessons.

Our Approach in This Guide

Since Lafley and Martin’s waterfall strategy must be followed in the order they wrote it, we’ve largely kept their structure. However, since Chapters 7 and 8 both describe how to apply the five questions of the waterfall strategy, we’ve combined them for brevity and ease of access.

We’ve also removed a great deal of the P&G case studies and stories while keeping the core lessons and using our commentary to make them as broadly applicable as possible. We’ll provide case studies and examples from different companies, thereby expanding the book’s view beyond Procter & Gamble. We’ve also included commentary that further enriches—and occasionally contrasts—Lafley and Martin’s ideas with connections to other iconic business guides, such as Richard Rumelt’s Good Strategy/Bad Strategy and Simon Sinek’s The Infinite Game.

Introduction | Chapter 1: Choices in Strategy

A.G. Lafley and Roger Martin—who worked together at Procter & Gamble between 2000 and 2015 as the CEO and a consultant, respectively—open by saying that most people don’t understand why some business strategies succeed and others fail. Without this understanding, they have trouble choosing a good strategy themselves.

However, Lafley and Martin assert that developing a good business strategy is deceptively simple: It’s the process of making tough choices that puts you ahead of the competition. These choices can confine you—making one choice often means forgoing another one—but they’re necessary for success. The key to finding a good strategy is learning how to win rather than just how to play.

The authors add that all employees, from the CEO to a retail salesperson, have to make strategic choices. Furthermore, they have to make those choices not just with the intent to compete, but to win. Winning will look different for different segments of the company: On the company level, it may include becoming the number one player in the market; on an individual level, it may mean having the best sales numbers in a region.

In Playing to Win, Lafley and Martin explain their system for designing winning strategies, which they developed at P&G. The authors call their system the “strategic choice cascade” to illustrate how each step flows into the next. For this guide, we’ll use the term waterfall strategy instead, which is simpler and more intuitive.

In Chapter 1, Lafley and Martin give a high-level overview of their system, which is based on five questions. Chapters 2 through 6 each focus on one of those questions, explaining what the question means and why it’s important. Chapter 7 guides you in working through the waterfall process yourself. Finally, the conclusion provides guidelines for determining whether the strategy you’ve created is a good one.

(Shortform note: In Good Strategy/Bad Strategy, Richard Rumelt offers a different definition of good strategy: using your strengths against weaknesses. This could mean using your strengths against your competitors’ weaknesses in order to get an advantage, or using your strengths against your own weaknesses in order to fix them. To integrate that definition with Lafley and Martin’s, a good strategy means making tough choices about what your strengths are, and where to apply them.)

The Waterfall Strategy

In Playing to Win, Lafley and Martin outline their concept of a “good” strategy that involves making winning choices—the waterfall strategy: an action plan for success in business.

The authors’ waterfall strategy entails answering five questions:

- What is your business’s vision and purpose, or your “winning aspiration”?

- What are your target markets?

- How do you succeed in those markets?

- What capabilities does your company need in order to “win,” or achieve its purpose?

- How should you manage your company in order to achieve its purpose?

Starting at the highest level, each question informs the next (hence the waterfall analogy) while also helping to refine the answers to the previous questions. As you work through the waterfall and gain new insights, you’ll revisit and refine your answers to previous questions.

Keep Your Answers Concise

While these five questions form the foundation of Lafley and Martin’s waterfall strategy, it’s important not to get bogged down in pursuing too many different answers to them. Pursuing too many options, or options that work against each other, is a common reason many business strategies fail. Instead, make only a few specific choices that, taken together, form a clear and cohesive strategy to reach your goal.

The authors add that, in large companies, many individual choices and broader strategies function at once and in conversation with one another. For example, one employee’s strategy could play into a brand strategy, which in turn connects with a larger sector strategy, which forms part of the overarching company strategy. Each strategy flows together to form a cohesive strategy that determines the overall success of the company—the authors call this a “nested cascade,” a waterfall made up of smaller waterfalls.

This guide will detail how companies can win at each level along the waterfall. First, we’ll explore each step of the waterfall in detail. Then, we’ll look at how to develop a system of decision-making that increases your company’s chances of winning, or dominating its market.

(Shortform note: In his business guide Good Strategy/Bad Strategy, Richard Rumelt asserts that simply having a strategy gives you an advantage over many other companies, who operate reactively or with only vague long-term goals. In other words, no matter what your specific strategy is, having a clear set of goals and guidelines puts you in a stronger position by default than many of your competitors.)

Misconceptions About Strategy

Lafley and Martin believe that businesses often struggle with strategy because they misunderstand what it is. They describe several common misconceptions:

1. Strategy is just a vision. Vision statements are good, but often there’s no action plan to back them up. There’s no point in having a vision if you don’t have a way to realize it.

(Shortform note: In Good Strategy/Bad Strategy, Rumelt adds that companies sometimes think vision and motivation are all you need for a good strategy, as if you can realize your goals through sheer dedication and force of will. Like Lafley and Martin, he says this approach is incorrect: Dedication and determination are excellent values, but they’re not aspects of strategy.)

2. Strategy is just a plan. A step-by-step plan is fine, but it’s not enough on its own to secure an advantage in the marketplace. A good strategy is goal-oriented and flexible enough to adapt to changing circumstances.

(Shortform note: Rumelt says that, in creating a goal-oriented strategy, it’s important to choose appropriate goals (he uses the term “objectives”). Like Lafley and Martin, Rumelt warns against splitting your focus among too many different goals, and he adds that each of your goals should be a clear step from your current situation to your desired situation.)

3. A long-term strategy is a waste of time. Many people think the world changes so quickly that long-term planning is impossible. This makes them reactive rather than proactive, which puts them at a disadvantage against more strategic competitors.

(Shortform note: In creating a long-term strategy for your company, there are certain challenges that you’re sure to face, such as competition, distribution, and advertising. Rumelt says that one common planning pitfall is failing to clearly and specifically identify inevitable challenges, which makes it impossible to overcome them.)

4. Strategy works within the status quo. A lot of companies try to optimize their strategy for the current situation, or else rely on “best practices,” instead of innovating new approaches to anticipate and meet customer needs. Again, this makes them reactive instead of proactive.

(Shortform note: One reason this is such a common strategic pitfall is that people tend to resist change—we’re inclined to uphold the status quo even if we know that better alternatives are possible. Therefore, companies are unlikely to pursue bold strategies that break with currently accepted theories and best practices.)

Chapter 2: Envision Your Company’s Ideal Future

The next five chapters will take you through Lafley and Martin’s waterfall strategy, question by question.

Question 1: What is your company’s ideal future? (In the authors’ terms, your “winning aspiration”)

To answer the first question, which starts the waterfall, figure out your definition of success and what you want your company to achieve. The answer, your ideal future, can include a statement of purpose, but it’s not only a statement of purpose. It’s also a statement of what success—or “winning”—would look like at your company. Once a company understands what it wants to achieve, it can take clear and specific actions toward that ideal future.

Lafley and Martin say that your goals must involve serving and pleasing your customers: If consumers like your company and your products, then you’ll naturally succeed in the marketplace. The authors add that focusing exclusively on internal issues (like profit margins, or marginal improvements to your products) will blind you to external market demands and make you less likely to reach your ideal future.

In other words, Lafley and Martin say that to figure out your ideal future, you have to determine what your business is really about—not just what you do, but why you do it. The authors say that, generally, companies will tell you their business is their product or service. In reality, though, all successful companies are in the business of meeting customer needs—the product or service is just the vehicle. For example, is a bar really in the business of serving alcoholic beverages, or is it providing a way for people to unwind and socialize?

(Shortform note: In Start With Why, Simon Sinek tells us why it’s crucial to understand the reason behind your business: Your product or service (your what) engages people’s rational minds, but your purpose (your why) engages their feelings. He adds that emotion-based decisions are reached more quickly and are less prone to outside influences than logic-based decisions—in other words, if a customer buys a product just because they like it, they’ll make that decision faster and feel more secure in it than if they buy a product because they researched and compared numerous similar products and decided on the “best” one.)

To figure out how to best serve your customers, first research what the customer needs, then tailor your company to meet that need better than anyone else.

The Three Perspectives of Business

Your customers’ needs are just one of three critical elements that must be addressed in a successful business strategy:

The customer: Who is buying your product?

The investor: Who is covering your costs?

The producer: Who is making your product?

Many business plans fail because they only consider the perspective of the producer—the company making the product or providing the service. Such narrow business plans tend to gush about groundbreaking technologies and revolutionary ideas, but overlook the fact that they’ll need people to invest in those innovations—and, even more importantly, they’ll need people who want to buy them.

That’s why Lafley and Martin say to begin with customer needs: First identify the need, and then determine how your great new innovation will allow you to meet that need better than anyone else does.

The Importance of Playing to Win

Lafley and Martin say that you must play to win because it’s hard to win. Many companies that want to win still lose. So, if you’re just trying to compete rather than dominate, you’ll have no chance at all—you won’t devote the time and resources necessary to stay in the game.

(Shortform note: In The 10X Rule, Grant Cardone also discusses the importance of trying to dominate rather than merely compete—but for different reasons: Cardone says that if you’re in a competition mindset, you’ll waste time watching your rivals and copying what they do, which is a recipe for failure. While Cardone does urge you to learn from your competitors, he warns against trying to emulate them or directly compete with them. Instead, with a mindset of domination rather than competition, look for the next great innovation that’ll let you completely bypass your competitors and corner the market.)

In any market, you’re naturally going to have competitors, many of whom will also have developed ideal futures and effective strategies to reach them. Therefore, Lafley and Martin suggest honing your strategy by identifying the competitor that is most formidable. Then ask: What are they doing that I’m not? How are they serving people better than I am? How can I overtake them?

Note that your strongest competitor might not be the most obvious one. For example, if you’re running a tech startup, it’s unlikely that you’ll be directly competing with Microsoft or Google right off the bat. Your strongest competitor in that case might be a much smaller company that’s targeting the same section of the market as you.

Respect Your Competitors

In The Infinite Game, Simon Sinek suggests viewing your competitors not just as rivals, but as worthy rivals. It’s a fine distinction, but Sinek believes that it’s an important shift in mindset: Respecting your competitors’ abilities means that you won’t just try to win, you’ll work harder to become good enough to win.

Imagine yourself as a boxer with an upcoming match. If you don’t respect your opponent, you won’t train as hard before the match—you won’t think it’s necessary. However, if you believe that your opponent is a worthy rival, you’ll be motivated to work hard and improve as much as possible before stepping into the ring.

As Lafley and Martin say, one highly effective way to improve your skills is to study your opponent, see what he or she does better than you, and use what you learn to shore up your weaknesses.

Chapter 3: Find Your Target Market

Question 2: What are your target markets?

After you’ve figured out your winning conditions, it’s time to move on to finding your playing field. Lafley and Martin’s second question asks: On which battlefield will your company fight? Or, what audience do you want to target? This can include fighting for particular demographics, to be on specific media platforms (websites, TV networks, or magazines), or in ideal geographic markets. As we’ll discuss, where you decide to play should be based on the state of the industry you’re competing in and your own company’s particular strengths.

(Shortform note: In Blue Ocean Strategy, Renée Mauborgne and W. Chan Kim compare markets to areas of the ocean. A “red ocean” is a market that’s already crowded, where competition is fierce and success is unlikely—imagine blood in the water, and the predators that it will attract. Conversely, a “blue ocean” is a fresh and new market where there’s little or no competition. When developing your business strategy, it’s best to look for blue oceans rather than trying to compete in a crowded market.)

Choosing Your Targets

Lafley and Martin say there are a variety of choices to make regarding where and how you will compete. To identify your target market, they offer a few basic questions to consider, such as:

- Region: Where are you competing?

- Product: What are you offering your consumer?

- Consumers: Who are you targeting?

- Distribution: What strategy will you use to deliver to your consumers?

- Production: How much of the production will you be responsible for?

In answering these questions, think strategically. Don’t dismiss entire industries or demographics because they seem unattractive at first glance—there might be a small niche you can fill, or an unexpected tactic you can use to break in. Conversely, don’t rush too quickly into what you perceive as an untapped market; there may already be a strong competitor catering to that market in a way that you don’t immediately see or recognize.

Finally, the authors note that some questions about your target market are more important than others. The industry, the size of the company, and how long the company has been around all contribute to which questions are most important. For example, large corporations might have to answer questions about which distribution companies are best in different parts of the country (in other words, how they’ll get their products to their target markets), or whether they should take their business international. Meanwhile, a long-standing company might consider broadening its target audience if its products are suddenly struggling in the company’s current market.

(Shortform note: Before starting a new business venture, entrepreneurs should ask additional questions, such as, “Will this be sustainable?” When picking your playing field, it’s important to choose one that you can not only break into, but can continue to succeed in. For example, if your strategy falls apart the moment you have serious competition in your chosen market, it’s not sustainable and therefore it’s not a good playing field for you. Similarly, if the costs of production, distribution, or advertising are unsustainable, then you need to target a different market.)

Avoid Playing Field Pitfalls

Lafley and Martin warn of three common pitfalls when considering what playing field to choose and how to choose it:

Pitfall #1: Not choosing at all—All companies need to be specific about their demographic choices, because trying to be different things to different people is a recipe for disaster. For instance, it’s very difficult to capture the attention of a young American man and an aging French woman at the same time. So, based on your company’s capabilities, decide what specific age groups, geographies, or channels (for example, mass merchandise vs. luxury) you want to cater to.

In other words, choosing where not to play is just as important as choosing where to play.

(Shortform note: One way companies make this mistake is by selling what marketing guru Seth Godin calls “mass products”—that is, products designed to appeal to everyone. In Purple Cow, Godin says that such products are bland and boring by design, because their goal is to be inoffensive rather than extraordinary. In short, the more you try to broaden a product’s appeal, the less appealing it actually is. This also plays into Lafley and Martin’s point about competing rather than dominating: Mass products try to play by the same rules that everyone else is playing by, while extraordinary products dominate the game by offering something new.)

Pitfall #2: Spending your way out of a bad situation—If your current playing field isn’t working out, don’t just spend more money and hope that somehow fixes the problem. Instead of funneling more resources toward a problem, you need to either shift your focus to a different market or fix the problem you’re having in the current one.

(Shortform note: In Rework, David Heinemeier Hansson and Jason Fried also caution against throwing money and resources at a problem in an effort to fix it. In fact, they suggest the opposite: Cut back on what you’re devoting to that particular issue, because that will force you to make difficult but crucial decisions about how to proceed. For example, you might find it necessary to reduce your workforce, sell off some resources, or even abandon a market entirely.)

Pitfall #3: Believing that choices are final: Some companies think there are certain places and ways that they have to compete. However, this isn’t true in practice: Many successful companies can and do change their playing fields when needed. For example, Starbucks started out selling coffee beans and espresso machines in the 1970s, then shifted in the 1980s to their current model of acting as a pseudo-European cafe—a move that led to Starbucks dominating the coffeehouse market today.

(Shortform note: In Rework, Hansson and Fried warn that one of the worst things a business can do is become paralyzed by indecision; they say that making a bad choice is better than making no choice. One way to avoid paralysis is by remembering, as Lafley and Martin say, that your decisions don’t have to be final. If it turns out that you did make a bad decision, learn from that mistake and make a different choice for the future.)

Exercise: Figure Out Your Target Market

This exercise will help you figure out the playing field for your product. Think of a product you sell (or would like to sell) then answer the following questions.

Where (physically) are you competing? (For instance, are you selling the product in local shops, or online?)

What products are you offering to your customer?

Describe your ideal customer. Based on this description, what is your target demographic?

How will you deliver your product to your customers? (For example, will you sell the product directly or through a distributor?)

Now, reflect on the playing field choices that you’ve made. How likely are they to help your product dominate your chosen market?

Chapter 4: Win in Your Arena

Question 3: How do you succeed in your chosen markets?

We’ve discussed how to figure out what you want and which market to target. Now, Lafley and Martin explain how to find a competitive advantage in your chosen market. You need to create sustainable value for customers.

Lafley and Martin say that there are two main ways to harness your strengths and find victory in your chosen market: cost leadership (beating your competitors’ prices) and differentiation (offering something your competitors don’t). Different companies have different strengths that contribute to their ability to excel in unique ways. For instance, small companies can often provide a more targeted, boutique service (differentiation) while larger companies can often deliver quality products at a more competitive price point (cost leadership).

(Shortform note: In Purple Cow, Godin makes the case that the only way to succeed is with a remarkable product or service that attracts attention. He uses IKEA as an example of standing out through cost leadership: By selling mass-produced, disassembled furniture in easy-to-stack boxes, the company greatly reduces production and shipping costs. As a result, IKEA can sell furniture much more cheaply than its competitors. Though IKEA is a large company today, originally it was innovation rather than size that allowed it to beat the competition on prices.)

Let’s discuss these two strategies in more detail.

Strategy #1: Cost Leadership

In this approach, you win by selling a similar quality product at a cheaper price than your competitors.

Lafley and Martin say that if three companies have products that are essentially the same, customers will buy the cheapest of the products. Companies that spend less to make their products have more flexibility on pricing. Therefore, the company that can make the product most efficiently can sell it at the lowest price and control the market.

Furthermore, according to Lafley and Martin, the company that makes the product in the cheapest manner can use this advantage in other ways. For example, the company could instead sell its product at the same price as its competitors and use the extra profit to pay for bigger marketing campaigns or more prominent shelves at the store, thereby increasing sales.

(Shortform note: In extreme cases of cost leadership, large retailers will drive their competition out of the market by intentionally setting prices so low that smaller companies can’t possibly match them. The large retailers absorb the temporary profit losses, while smaller companies can’t and go out of business. Then, once the competitors are gone, the large company raises its prices to recoup the losses and increase long-term profit. This particular type of cost leadership is called predatory pricing.)

Strategy #2: Differentiation

Lafley and Martin’s alternative to lower prices is having a product that consumers want more than others because it’s of higher quality or has better branding and more prestige. If it costs two companies the same amount to make similar products, but consumers like one more than the other, they’re willing to pay more for it. This leads to higher margins that companies can then use to increase their advantage through higher-priced marketing campaigns or better placement in stores.

Selling a quality product can also help develop loyalty, which makes a company less vulnerable to the whims of the market: Loyal consumers believe that a particular company adds value to their lives, so they don’t shop around as much.

The Elements of Brand Loyalty

Brand loyalty has two main components:

Popularity: People assume that the top-selling brands must be the best quality, and they become loyal to those brands without exploring other options.

Personality: People are attracted to brands when the advertising and presentation matches their personality, or how they see themselves. For example, Red Bull and Monster are two popular brands of energy drink—Red Bull advertises with silly, cartoonish commercials, while Monster presents itself as intense, athletic, and powerful. By using two different approaches, these brands capture different sections of the energy drink market.

Employing These Strategies

Sometimes, Lafley and Martin add, a firm can use cost leadership and differentiation strategies at the same time—driving down the cost of manufacturing and keeping their prices low while still driving up comparative quality. However, this is difficult to pull off unless your company already dominates the market to the point that it can afford to split focus among two different strategies, so most companies have to choose one strategy or the other.

Lafley and Martin point out that companies aiming to be cost leaders must strategize and sacrifice differently than companies that are aiming to be differentiators:

- Cost leaders prioritize cheap production and low prices, so they might alienate customers who are interested in something that’s unique or different.

- Differentiators prioritize building the brand to be customer friendly, fresh, and attractive. This often results in more expensive products, which drives away customers whose primary concern is cost.

Counterpoint: Amazon Successfully Pursues Both Strategies

Amazon is one example of a company that manages to be both a cost leader and a differentiator. In The Everything Store, which tells the story of Amazon from its founding in 1994 to the 2010s, journalist Brad Stone explains that founder Jeff Bezos has an “obsession” with customer service. However, for Bezos, part of serving the customer is pricing the product as low as possible. That’s why, in addition to looking for other ways to boost customer satisfaction, Amazon is always on the lookout for ways to reduce its prices—including (according to Stone) predatory and legally questionable practices to avoid taxes and drive competitors out of the market. While maintaining cost leadership, the company differentiates itself by using technology and continuous innovation to meet customer needs.

Its success as both a cost leader and a differentiator has made Amazon a regular in the Fortune 100, as well as one of Fortune’s “Big Five”—the five most influential tech companies in the US. This example shows that it’s possible (if difficult) to excel at both strategies, but doing so successfully can give you an enormous competitive advantage.

Strategize at Every Level

Lafley and Martin warn that some companies think only workers who are customer-facing need to understand and employ strategy. However, having winning strategies at every level of the organization, both outward-facing (like sales) and inward-facing (like product development), will help any company succeed, regardless of whether you’re trying to be a cost leader or a differentiator. Therefore, every part of your business should consider the “where to play” and “how to win” questions we’ve previously discussed.

Crowdsourcing Strategy

For an example of what it looks like to strategize at every level, Netflix CEO Reed Hastings took an exceptional approach to company strategy by encouraging every single Netflix employee to innovate and contribute to the overall plan.

In No Rules Rules, Hastings explains that there were three steps to this process:

Hire the right people—at any cost. Hastings’s strategy for Netflix was based on employee independence and autonomy. In order for that strategy to work, he needed to hire trustworthy people who wouldn’t abuse their privileges.

Encourage open communication and feedback at every level. Hastings taught his employees how to give and take feedback effectively, then encouraged them to constantly provide feedback to him and to each other.

Remove employee restrictions. Hastings removed top-down controls like strict approval processes (while still providing guidelines to prevent abuse). His employees were not only encouraged but expected to take responsibility for themselves and their own projects.

According to Hastings, these three steps—along with a company culture of innovation and accountability—empowered Netflix’s highly skilled employees, which fostered the ingenuity and adaptability that enabled the company to grow into the streaming giant it is today.

Strategize Constantly

Lafley and Martin explain that some companies gain such a significant competitive advantage that they’re able to push their competitors almost entirely out of the arena—consider Google and Amazon, which have no serious competitors in their respective markets.

However, the authors warn that markets change constantly and strangleholds don’t always last. That’s why even ultra-successful companies can’t afford to rest on their laurels; they must constantly create and employ new how-to-win strategies so they don’t get overtaken by new and innovative competitors.

(Shortform note: In contrast to Netflix’s constant innovation at every level, Blockbuster Video is a perfect example of a successful company that grew complacent. In 2000, the then-CEO of Blockbuster had a chance to buy Netflix for $50 million. Thinking that Blockbuster was comfortably at the top of the video rental market, and that Netflix was a harmless novelty, he declined the offer. Just 10 years later, Blockbuster declared bankruptcy—Netflix and similar services forced it out of the market it had once dominated.)

Exercise: Engineer Success

Develop your ability to find your playing field and figure out how to succeed in it.

Describe a product that your company sells or would like to release.

Who is your product’s competition?

Is cost leadership or differentiation the better strategy for the product based on your competition? Why?

Chapter 5: Build Ingredients for Success

Question 4: What capabilities does your company need in order to win?

Lafley and Martin say that once you’ve decided where you’re going to play and how you’re going to win, the next step is figuring out what resources and skills you need to achieve your victory—in other words, what capabilities your company will need, such as innovation, efficiency, or leadership. To do so, determine what your company needs to be good at—and what it needs to be the best at—in order to win in the playing field you’ve chosen.

(Shortform note: Lafley and Martin suggest that you start by coming up with goals, then figuring out what capabilities you’ll need to reach those goals. However, some business strategists suggest the opposite: Start by determining three to six things that your company already does well, invest your time and resources into further improving those capabilities, and base your business strategy around those.)

Determine and Map Your Capabilities

Lafley and Martin say that a successful strategy requires you to identify the capabilities you’ll need to reach your goals within the context of your where-to-play and how-to-win choices. These core capabilities must not only work in concert but also reinforce each other. (Shortform note: A 2014 survey of companies worldwide found that more than half named building capabilities as one of their top three priorities, but only 18% have objective systems of identifying their capabilities.)

The authors suggest creating a visual representation of these capabilities and the activities that support and branch out from them; this map is called an activity system. Mapping an activity system can also help you figure out methods to build and support necessary capabilities. The final result should look something like a web, with a few key goals connected to numerous capabilities and plans for building those capabilities.

At this point, the authors advise asking yourself how feasible your activity system is: What new capabilities would your company need to build, and how expensive would it be? If your goals are too costly to pursue, then you need to rethink your playing field, how you’ll win in that field, or both.

How Strong Is Your Web?

Another benefit of activity maps is that they allow you to see how closely related your business goals are to one another. If the same capability supports multiple goals (even indirectly), then those goals are aligned with each other and will synergize well in your overall strategy. If your activity system creates a dense, tightly connected web, then you have a strong business strategy. Conversely, if your goals and capabilities are scattered and disconnected, you may need to rethink your approach.

Example: Southwest Airlines

StrategicToolkit.com shows an activity system from Southwest Airlines as an example. The system shows the company’s goals (how they plan to win) in yellow, and what they need to reach those goals (capabilities and methods) in white. This is a strong and well-connected activity system, with many capabilities linking to multiple others and supporting different goals through clear, well-planned paths.

Make Your Activity System Unique

Lafley and Martin say that your activity system should be distinct from your competitors’. If your web and theirs are too alike, they could imitate your strategy and cause you to lose your competitive advantage.

This doesn’t mean that any individual activity in your system has to be unique or impossible to replicate—rather, the combination should be one-of-a-kind. For example, no other company has been able to replicate Taco Bell’s activity system built around cheap, convenient Tex-Mex food and worldwide distribution.

(Shortform note: While Lafley and Martin advise you to study your direct competitors, some business consultants suggest a broader view: Learn from the very best, no matter what markets they compete in. For example, if you’re trying to build up your company’s capacity for creativity, you could study companies like Google, Amazon, and Netflix—world leaders in innovation.)

Identify Brand-Specific Capabilities

So far we’ve focused on companywide activity systems. Lafley and Martin say that for small companies with just one brand or product, this might be the only activity system you need to worry about. However, for larger companies with multiple brands, each brand needs a unique system of capabilities that ensures success in its own arena.

To build up the unique capabilities of each of your brands, Lafley and Martin suggest you:

- Begin at the individual level. Start with building an activity system of one indivisible brand, where every product requires the same activities. For example, Pepsi makes many different soft drinks, but each product has the same inherent system because they all share the same management, the same production, the same distribution, and so on.

- Build competitive advantage at the aggregate level. After you build activity systems at the indivisible brand level, focus on brands that are similar and therefore able to share resources, skills, and knowledge. This increases the efficiency and competitive advantage of both brands by combining their capabilities.

- Figure out how your systems are working, and expand or contract accordingly. Once you’ve created the systems for brands to share capabilities and knowledge, you may realize that your company needs to expand (create or acquire more brands with capabilities that reinforce company goals) or contract (sell off brands with unneeded capabilities).

(Shortform note: As the CEO of Procter & Gamble, Lafley practiced what he preaches in regard to brands. He spent a great deal of money to acquire new brands, strengthen the brands he already had, and cut loose the brands that would do better on their own. The result is that P&G now rests on a strong foundation of “superbrands,” a small collection of the company’s most successful brands, made even stronger by increased investments in them. The goal was to make P&G more resilient to market shocks and uncertain times.)

Build Capabilities Through Acquisitions

Lafley and Martin say that when organizations don’t have the necessary capabilities to achieve their goals, they often think the easiest way to build those capabilities is to acquire another company. However, even though mergers between two big corporations are increasingly popular for this reason, most end up being unsuccessful—the combined profit ends up being less than the sum of its parts because the companies or brands don’t work well together.

When discussing mergers or acquisitions, companies often talk about synergy between each other, but Lafley and Martin stress that synergy begins with strategy: If another company fits into your overall strategy, then it will be a good target for acquisition and will naturally synergize with yours; if not, then it’s not worth acquiring, no matter how impressive its capabilities are or how big and loyal its customer base may be.

In other words, think carefully about your overall strategy and how a potential new acquisition will help you carry it out before taking the next step. Don’t snap up other companies just because you can.

The Spirit of the Strategy

Sometimes the reason a merger fails isn’t that the new company doesn’t fit your strategy, but that the new company doesn’t fully understand what your strategy is. The most common issues with failed mergers come from misunderstandings and “benign neglect.” In other words, people have different understandings of what they’ve agreed to, and they don’t realize it until it’s too late.

When one company acquires or partners with another, these misunderstandings and disagreements can lead to a new whole that’s less than the sum of its parts—what Lafley and Martin call an unsuccessful merger. That’s why it’s crucial to make sure that everybody’s clear on the spirit of the agreement, not just the terms of it. For example, if your plan is to take the best capabilities of both companies and liquidate the rest, make sure your new acquisition understands that you’ll be closing down sites and laying off employees to carry out that streamlining strategy—the last thing you want is for the company to push back when you start implementing your plans.

Exercise: Determine Your Capabilities

This exercise will help you determine and develop the capabilities necessary for success.

Think of a product you’ve launched or would like to launch. Briefly outline what this product is.

What are the capabilities associated with this product? Which of these capabilities are stronger than your competitors’?

Based on your strongest capabilities, what is the most appropriate market for your product? In what ways are your capabilities particularly suited to this market?

What capabilities will you need to develop to dominate this market? (Think of the resources, skills, information, and people you’ll need to succeed.)

Chapter 6: Organize for Success

Question 5: How should you manage your company?

It’s tempting to believe that if you complete the previous steps—determine your aspirations, a place to play, a way to win, and the capabilities to fulfill all of those goals—then your company will succeed. But Lafley and Martin warn that, while those steps are important, a successful company also needs three management capabilities to make sure the rest of the waterfall flows smoothly:

- Systems to review strategy

- Systems to communicate strategy throughout the organization

- A system to measure progress

The Challenges of a Work-From-Home Team

With the coronavirus pandemic, and the resulting increase in teleworking, these capabilities are more important than ever. Managing a work-from-home team or a hybrid team (where some employees are in the office and some aren’t) presents unique challenges. Specifically, fairness and communication are the keys to effectively managing such a team. That’s exactly what the capabilities listed above accomplish.

Clear systems for measuring progress and performance ensure fairness at both the individual and the company level: Everyone will be held to the same standards, regardless of where they work from. Clear communication structures—both top-down and peer-to-peer—ensure that your employees at home aren’t left out of the loop.

Furthermore, each of these three management capabilities requires a clear and specific structure to support it.

Capability #1: Systems to Review Strategy

Lafley and Martin say that a healthy work environment—one with good communication and happy employees—is necessary for strategic success. The CEO needs to be able to have an open and collaborative relationship with those working under him, and so on, all the way down to low-level managers and employees. To foster this collaboration and deftly respond to new challenges, managers and executives must discuss issues and review strategy in the open.

According to Lafley and Martin, the best way to do this is to have regular open discussions. Focus on simple strategic questions during these discussions, and don’t expect to come up with a perfect plan in one fell swoop—strategy is a continuous process of innovation, discovery, and review.

If your company isn’t used to open strategic discussions, Lafley and Martin warn that implementing them may be a difficult process. People are taught to work in a certain way, and it’s not easy to start receiving and giving feedback in a different way. However, if you emphasize this new, interactive meeting style over a period of months, your team will adjust and come to enjoy it.

As an added benefit, people will start to think more about the strategy of the company. Lafley and Martin assert that when people have to defend their ideas with a detailed presentation, they’re more likely to be concerned about presenting well than formulating strategy. With open discussions, the pressure of presentation is removed, and people feel more confident about suggesting new strategies and contemplating the options.

Open Discussions Start With Trust

Open discussions of this nature require trust: Each person in the discussion must trust the overall company strategy, and also trust his or her coworkers to be respectful and honest.

According to Simon Sinek’s book Start With Why, trust isn’t a rational feeling, and isn’t tied to actions; rather, it’s tied to values. Therefore, to make these open discussions productive, you first need to build trust by demonstrating to your employees that you share their values and their concerns.

For someone in a leadership position, this means giving your team a compelling shared cause or goal—something they can work toward, instead of just working on. If everyone believes that they’re working toward the same goal, they’ll naturally develop a shared trust that gives them the courage to speak up and take risks in open discussions, which will lead to more productive meetings and effective strategies.

Set Guiding Principles for Open Discussions

Lafley and Martin add that open discussions are useful for crowdsourcing ideas, finding weaknesses in your strategy, and building your team’s enthusiasm. However, the authors also warn that open discussions can be counterproductive if people have different ideas about what your company or team is trying to accomplish.

To avoid confusion and ensure that everyone’s working toward the same goals, create a standard set of principles for strategic discussions. These principles should keep people focused on the company’s goals and its winning strategy.

(Shortform note: Interestingly, in Built to Last, the authors note that the success of a company might actually hinge more on how well they keep to their principles than on what those principles actually are. Their evidence is that the world's most successful companies don’t share all of the same principles, but they do share a commitment to upholding those principles at every level. This may have to do with trust, as Sinek says in Start With Why—if you have a reputation for sticking to your principles, then your employees and customers will trust you, which will lead to greater success in business.)

Capability #2: Systems to Communicate Strategy

Since Lafley and Martin emphasize that a successful strategy is developed and enacted at every level of an organization—from the CEO to low-level employees—company leaders must communicate the organizational strategy to everyone.

First, executives need to make the message compelling by distilling the few elements of the strategy that are key to the company achieving its goals. These elements will reflect the answers to the first four questions of the waterfall strategy: the company’s ideal future, its target market, its arena (cost leadership or differentiation), and its capabilities.

Second, leaders must communicate the strategy in clear, simple language. This makes it easier for employees to remember and carry out the strategy.

(Shortform note: When a company strategy is unclear or doesn’t resonate with employees, they don’t do their part to execute it, rendering the strategy virtually useless. To close this communication gap, many CEOs are appointing chief strategy officers (CSOs) to not only develop organizational strategies but also ensure that every employee understands the strategy and their individual role in it.)

Capability #3: A System to Measure Progress

Lafley and Martin say that it’s hard to keep generating ideas for new strategies if you don’t have a clear sense of how much progress you’re making. Especially in a big company, it’s difficult to see how your ideas are implemented and how they affect the company’s bottom line.

Therefore, when you create a strategy, establish expected outcomes and a way to measure results against those outcomes. Invest in measuring systems that deliver reliable data on your company’s performance. Use that data to determine what’s working, what isn’t, and how you can improve your strategy.

Lafley and Martin warn that you should never use a single outcome to determine your success. Establish individual goals for each department to ensure your company’s overarching strategies are well-rounded, and that one missed goal doesn’t derail your motivation or morale.

(Shortform note: When setting goals, make sure that they’re appropriate for each individual department or employee, not just a “company standard.” For example, an innovative new unit within your company shouldn’t be held to the same standards as a long-established and optimized core business unit; doing so just sets that new unit up for disappointment and failure.)

Chapter 7: Work Through the Waterfall

Now that we’ve covered the five steps of Lafley and Martin’s waterfall strategy, we’ll delve into exactly how to make decisions at each step. There’s no surefire formula for victory, but there are frameworks that, if used correctly, can serve as jumping-off points and make success more likely.

Leverage Uncertainty Through Options

Lafley and Martin say that there’s no sure way to win in the marketplace because there are always unknown variables and uncertainty in any strategy. In Antifragile, statistician and risk analyst Nassim Nicholas Taleb explains how to make uncertainty work in your favor instead of against you.

One of Taleb’s key points is to always leave yourself as many options as possible; every option you have available helps you to maximize opportunities and minimize harm from any sudden changes. For example, if you’re considering reducing your staff to save on overhead, keep those workers around for as long as is feasible—you’ll always have the option to let them go later. That way, you’re ready for one of two possibilities:

If the market improves and there’s a sudden increase in demand, you’ll have trained and experienced staff ready to take full advantage of it.

If the market suffers, you can proceed with the layoffs to minimize your losses.

In the meantime, the only cost of maintaining that option is the same salaries that you’ve been paying them the whole time.

While you work through Lafley and Martin’s waterfall strategy, remember that no decision is final. Each step of the waterfall affects all the others (not just those below it), and every strategy can change based on shifting market conditions. Therefore, even following this guide, you’ll most likely come back to the early steps and rethink the decisions you make.

Remove Ego From Your Decisions

When responding to changing circumstances, one unforeseen obstacle can be your own sense of pride. In Ego Is the Enemy, Ryan Holiday explains that pride (or ego) can prevent us from recognizing when we’ve made a bad decision or admitting that we need to change our approach.