1-Page Summary

Successful companies who pay attention to what their customers want and invest their resources in what generates the most profits usually continue to succeed. However, when a disruptive innovation shakes up an industry, these normally sound business practices can drive established market leaders to fail. This phenomenon is what Harvard Business School professor and leading expert on business innovation Clayton M. Christensen calls “the innovator’s dilemma.”

In The Innovator’s Dilemma, Christensen first presents a theory to explain why disruptive innovations can cause business practices that normally bring success to bring failure instead, and then offers advice on how to adopt disruptive innovations successfully. Christensen published the first edition of The Innovator’s Dilemma in 1997, during the height of the era’s tech boom. The book was hailed as one of the best business books not only of that year, but ever written, and it was quickly adopted as a resource for CEOs and management leaders.

In this guide, we’ll examine Christensen’s theory and advice, and we’ll contrast it with the perspectives of other experts on the subject, such as Geoffrey Moore, W. Chan Kim, and Renee Mauborgne. Moore is the author of Crossing the Chasm, which addresses the same issue from the perspective of a start-up company trying to displace market leaders with a disruptive innovation. Kim and Mauborgne are the authors of Blue Ocean Strategy, in which they present a strategy for introducing disruptive innovations to reshape the market in ways that make your competitors irrelevant and give your company room to grow.

Why Disruptive Innovations Are Disruptive to Established Companies

To explore Christensen’s theory, we’ll first examine what a disruptive innovation is and the difference between disruptive innovations and sustaining innovations. Then we’ll discuss how these innovations disrupt markets and their characteristics that create problems for established companies.

Disruptive Versus Sustaining Innovations

Christensen defines a “disruptive innovation” as any new product that disrupts the mainstream market. For example, in the early 1900s mechanical tractors took over the draft-horse market. He also calls “disruptive innovation” a “discontinuous” innovation because it causes previous technologies or business practices to be discontinued.

Christensen explains that typically, a disruptive innovation involves a drastically different approach to doing something, which, at first, doesn’t appeal to mainstream customers. Instead, it appeals only to a developing niche of customers with different needs. However, as the new product becomes more refined, its capabilities increase to the point where it offers greater value than traditional options in the mainstream market. At that point, he says, mainstream customers begin adopting it en masse, disrupting the market.

Christensen contrasts disruptive innovations with “sustaining innovations,” which he defines as incremental improvements to a product that don’t alter the market. For example, an early tractor manufacturer might switch from using two-cylinder engines to four-cylinder engines. This makes their tractors more powerful and efficient, but it doesn’t change who buys the tractors or why they buy them. Sustaining innovations are also called “continuous” innovations.

Comparing Definitions of Disruptive Innovation

Geoffrey Moore provides a slightly different definition of the difference between sustaining and disruptive innovations.

According to Moore, a disruptive (or discontinuous) innovation is any new product that requires the customer to change how he uses a product in order to adopt it. For example, a farmer who sells his plow horses and buys a mechanical tractor now has to buy fuel for the tractor instead of feeding hay to his horses. Instead of having a ferrier periodically put new shoes on his horses, he has to have a technician perform maintenance on his tractor. He has to develop new skills and work with different suppliers to make use of the new technology.

Similarly, according to Moore, a sustaining (or continuous) innovation is a product that is improved in some way but doesn’t require the customer to change in order to benefit from the improvement. For example, a farmer who upgrades from a two-cylinder tractor to a four-cylinder tractor can still buy fuel from the same supplier and have it serviced by the same technician.

Thus, to Moore, a disruptive innovation is disruptive to the customer’s life or routine, while to Christensen, a disruptive innovation is disruptive to the market. In principle, these are fundamentally different definitions. Hypothetically, if John Deere introduced an autonomous tractor that required farmers to learn C++ programming, and farmers gradually adopted it without disrupting the market, then Moore would call it a disruptive innovation, while Christensen would call it a sustaining innovation.

How Disruptive Innovations Reshape Markets

Christensen outlines the typical chronology by which disruptive innovations displace established companies:

- Someone invents a disruptive product, forms a start-up company, and begins producing it.

- Established companies evaluate the product and decide it wouldn’t be profitable in their current market, so they don’t pursue it.

- Through trial and error, the start-up finds an emerging market for their product.

- The start-up continues to refine their product. Eventually, its value (capabilities and reliability at its price point) surpasses traditional alternatives, and mainstream customers become interested in it.

- The disruptive product begins to dominate not only the emerging market that formed around it, but also the mainstream market, displacing traditional alternatives.

- Established companies realize that they are losing market share to the disruptive innovation, but by then it’s too late for them to defend their market share, even if they adopt the innovation themselves.

Comparing Chronologies

Christensen presents his chronology of disruptive innovations from the standpoint of a business analyst and advisor to established companies. Moore presents a similar chronology from the standpoint of giving a start-up company a battle plan for conquering the mainstream market. Let’s consider Moore’s chronology and compare it to Christensen’s:

You come up with a revolutionary product. (This is the first step in disruptive innovation according to almost any expert.)

You sell your first few units to curious customers who try it out and corroborate the claim that you’ve created a novel product. These early enthusiasts probably won’t buy enough for you to make much money, but they help you refine the product and get the word out to a broader audience by word of mouth. In Christensen’s chronology, this is step three. His step two says that established companies first reject the new product—a step that Moore, in this chronology, doesn’t address.

You connect with a few ambitious customers who see your product’s future potential. They want to use your product for something specific and have the capital to implement it. You sign a lucrative contract with them to improve and customize your product to meet their needs. A few such contracts make up the bulk of what Moore calls the “early market.” Moore’s “early market” corresponds to Christensen’s “emerging market,” so this step closely corresponds to Christensen’s third step.

You select a single niche application for your product and refine it to provide indisputably better value in that application, allowing you to become the market leader in that niche. This corresponds to the first half of Christensen’s fourth step, though he doesn’t mention niche applications explicitly.

You continue to refine your product and expand into an adjacent niche. Repeat. As you become the market leader in more and more sectors, eventually you dominate the entire mainstream market. This corresponds to the second half of step four and step five of Christensen’s chronology. At this point, Moore’s mission is accomplished, so he doesn’t go on to discuss the fate of the former market leaders that you displaced, as Christensen does in his sixth step.

Problems That Disruptive Innovations Cause for Established Companies

Why don’t established companies just embrace the innovation at step two and reap its benefits, instead of falling behind until step six? Christensen explains that there are a number of reasons established companies rarely adopt disruptive innovations before it’s too late.

1. Disruptive Innovations Get Started in Small Markets

As Christensen points out, it takes a big market to sustain a big company. However, when they first appear, disruptive innovations usually appeal only to a niche market that’s too small to be of interest to large, established companies. Thus, the companies that pursue disruptive innovations tend to be start-ups that are small enough to cater to small markets. If the market grows as the technology matures, the companies have a chance to grow with the market. However, by the time the market gets big enough for big companies to take notice, it may be too late for those larger companies to catch up.

(Shortform note: Marketing experts Al Ries and Jack Trout explain that in any given market, the first company to assume a position of market leadership in the minds of customers usually remains the market leader. Thus, market forces tend to prevent late adopters from claiming much of the market share, even in cases where the disruptive innovation doesn’t involve a significant technological learning curve.)

2. Disruptive Innovations Don’t Appeal to Existing Customers

Christensen explains that when a disruptive innovation first appears, an established company’s customers usually have no interest in it, because its performance characteristics are usually inferior to more mature technologies. Initially, the new innovation doesn’t compete for the same customers that buy the company’s current products. The few customers that it does attract have special interests that the new product uniquely addresses.

The Technology Adoption Life Cycle

Christensen says that the market for disruptive innovations usually starts out as a small, niche market. Others have also studied this phenomenon and developed models to explain it.

Probably the best-known model is the “Diffusion of Innovations,” which was originally developed by two agricultural scientists George Beal and Joe Bohlen. This model was generalized and popularized by Everet Rogers, and then refined by Moore, who called it the “Technology Adoption Life Cycle,” or TALC.

As Moore presents it, the TALC predicts that the market for any disruptive innovation is made up of five groups of people, who become interested in the technology at different stages of its development:

“Techies” or “Innovators” love new technology for its own sake. They buy new products just to try them out and are happy to tinker with things in order to make them work, but they only represent about 2% of the population.

“Early Adopters” or “Visionaries” see emerging technologies as opportunities to gain revolutionary capabilities before anyone else does. They represent about one-sixth of the population.

The “Early Majority” or “Pragmatists” hope to benefit by keeping up with the state of the art, but they only buy proven products from reputable companies. They represent about a third of the population.

The “Late Majority” or “Conservatives” don’t care about keeping up with the latest developments, but they don’t want to be left behind either. They tend to value simplicity, convenience, and affordability over performance. They make up about one-third of the population.

The “Laggards” or “Skeptics” are innately skeptical of anything new. They never buy new technology if they can avoid it. They make up about one-sixth of the population.

Thus, when a disruptive innovation is introduced, the first customers are the “techies,” and so the initial market will be limited to a few percent of the overall population. Meanwhile, the majority of an established company’s customers will be members of the early and late majorities, who don’t become interested until the innovation has been refined and standardized.

3. Disruptive Innovations Can’t Demonstrate Potential Growth

As Christensen points out, most established companies are under pressure to maintain a steady, positive rate of growth to keep their stock prices going up and thereby keep their stockholders happy. Therefore, when investing in a new product, companies are expected to promise substantial growth to justify their investment. However, even if a company recognizes that the market for a disruptive technology may grow as the technology matures, they can’t show their shareholders and investors market data on markets that don’t exist yet. This makes it hard for them to justify investing in innovations, because established companies are used to making strategic decisions based on sound market research.

(Shortform note: Compounding the problem of predicting which innovations may offer long-term growth and which will not is the fact that not every disruptive technology grows to take over the mainstream market. In fact, the majority of disruptive innovations only flourish briefly in an early market made up of techies and early adopters, after which they stagnate and die without making it into the mainstream market.)

4. Disruptive Innovations Require Retooling

Christensen asserts that established companies are often poorly positioned to produce or sell disruptive products because the new innovation takes a different approach, requiring different component parts or manufacturing methods. This, in turn, may require different supply networks. The company’s operations are tailored to its current products and thus are not optimized for new innovation. They may not even be able to accommodate it without an expensive overhaul.

For example, suppose a horse trader wants to start dealing in automobiles. The horse trader already has connections with ranchers and breeders who supply him with wholesale horses, but he’ll need to develop new relationships with automobile manufacturers. He also has stables to keep his horses in, and barns to store hay, but he’ll have to remodel them to store automobiles and spare parts. He currently pays stable hands to feed and water the horses every day, but that won’t be necessary with automobiles, so he’ll have to re-think his daily routines and operating procedures to keep his employees productive.

Retooling for Innovations in Sales Methods

This principle applies to practically all disruptive innovations, not just physical products. In The Challenger Sale, Mathew Dixon and Brent Adamson explain “solution selling,” a disruptive innovation in business-to-business sales: Instead of simply fulfilling purchase orders, you would sell the customer a complete solution customized to their needs.

But this changed the relationship between the customer and the salesperson. Instead of just delivering what the customer ordered, the sales rep had to assume a consultative role, challenging the customer to rethink their operations and showing them how they could benefit from a customized solution.

Dixon and Adamson observed that relatively few sales reps were able to transition to solution selling, because they struggled to mentally retool their role, just like a factory struggling to retool its production lines for a different product.

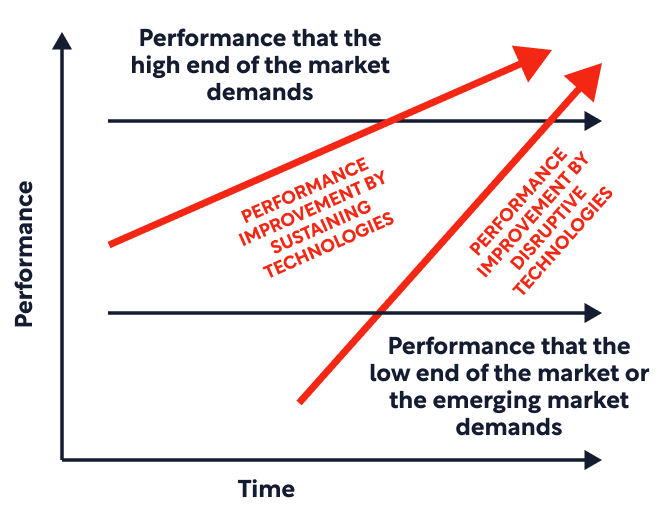

5. Disruptive Innovations Appear Down-Market of Established Products

Christensen argues that most companies tend to move up-market over time, appealing to increasingly demanding customers, and reaping higher profits from higher-end products as the company gains experience and refines its products. However, disruptive innovations usually start out down-market—they start out relatively simplistic and have to be priced at the lower end of the market spectrum.

(Shortform note: Al Ries and Jack Trout offer additional insight on why disruptive innovations start out down-market. They assert that budget-friendly versions of new innovations tend to sell better, because customers see the technology as unproven. The lower cost reduces the risk of buying it.)

Christensen points out that to adopt the new innovation, a company would have to shift its focus back toward the lower end of the market. This is financially problematic because of the lower profits per unit sold. It’s also culturally problematic, because it’s hard to give up the prestige that you’ve built up and start over.

Cross-Examining Up-Market Mobility

Do companies really tend to drift up-market over time as Christensen says? It makes sense that, as you gain experience with making a particular product, you’ll figure out how to make it better. In principle your product should move up-market as it improves. However, in practice, the marketing concept of positioning makes it difficult to move up-market or down-market.

Your “positioning” is how customers see your product or brand. For example, do they see you as the quality leader in your industry? Or the cheap knock-off? Or the environmentally-friendly option? Or the version made especially for a particular gender, age group, or other demographic?

Marketing experts assert that once customers have established your position on the market landscape, it is very difficult to change their perception of your product or brand. So if you start out selling entry-level products and customers recognize your place in the market, it may be difficult to move up-market, even if your quality improves over time.

What You Can Do to Adopt Disruptive Innovations Successfully

We’ve explained what disruptive innovations are, how they disrupt markets, and why they’re a problem for established companies. Now let’s examine Christensen’s advice on how established companies can overcome these problems.

Christensen’s recommendation is to establish an organization that functions like a small start-up within the parent company. This works because, as we’ve seen, most of the problems that prevent established companies from investing in disruptive innovations are irrelevant to small start-ups.

You can create the organization either as a spin-off of your existing operations, or by acquiring an existing start-up. Either way, Christensen stresses that the new organization must have adequate autonomy to explore and develop disruptive innovations. It will struggle if it has to compete for resources with the company’s sustaining-innovation projects, because it operates in an emerging market where there’s less opportunity for high-volume sales. It may also need to develop supply chains and operating procedures that are incompatible with those of the parent company.

(Shortform note: In Blue Ocean Strategy, W. Chan Kim and Renée Mauborgne argue that emerging markets with less opportunity for high-volume sales are actually the most secure path to eventual high-volume sales, as a company’s best chance to grow and succeed is when it operates in an uncontested market—as it would when introducing a disruptive innovation. They argue that although you may have difficulty in developing new supply chains and operating procedures, as Christensen mentions, your competitors will also. Thus, the challenges you might face as a start-up can end up being your strengths because they delay other players from entering the market.)

Christensen also stresses the importance of budgeting for multiple attempts at marketing the disruptive innovation. Recall that start-ups often have to find the emergent market by trial and error, because there’s no actual data on markets that don’t exist yet, which makes them impossible to accurately forecast. You may have to explore several different applications or niche markets before you find one where the product takes off.

Making Decisions Without Data

Moore echoes Christensen’s observation that emergent markets are hard to forecast because you can’t gather metrics on them yet. However, where Christensen advocates mitigating the uncertainty by budgeting for multiple attempts, Moore suggests using customer characterizations to guide your planning.

Each customer characterization is a description of a hypothetical customer, complete with information about their age, job, goals, and so on. These descriptions should be as realistic and as lifelike as possible. Once you’ve created profiles for the archetypical customers that might want your product, you use them to think through hypothetical purchasing scenarios: What does the customer’s current situation look like without your product? How would having your product solve her current problems? Is the improvement enough to compel her to buy?

By anticipating how each hypothetical customer would behave in each scenario, you can assess which customer would be most likely to buy your product. According to Moore, this method works because your intuition is much better at predicting how a person would respond to a situation than it is at predicting the behavior of abstract entities like markets. And when you’re introducing a disruptive innovation, you have to make decisions based on informed intuition, because you don’t have enough data to make an analytical decision.

Of course, these two methods are not mutually exclusive. When you’re operating in uncharted technological territory, it’s prudent to inform your intuition with customer characterizations and budget for multiple attempts whenever possible.

Managing an Acquired Start-Up (Or Spin-Off)

Like Christensen, business and marketing consultant Regis McKenna points out that collaboration between a large, established company and a small, innovative start-up organization can be beneficial because of their different strengths and capabilities. However, he also points out that their differences can make collaboration difficult, so much so that many attempts at collaboration end in bankruptcy for one or both organizations.

McKenna notes that collaboration can take the form of a joint venture, an acquisition, or any other agreement to work together on something. He doesn’t specifically mention collaboration between a parent company and a start-up-like spin-off organization within the company, but since this relationship is very similar to that of an acquired start-up, we infer that the same problems would apply.

McKenna identifies two keys to effective collaboration between a start-up and an established company:

1. Adequate separation. Both organizations must retain enough autonomy that they each have their own supply lines, customers, and unique culture. He warns that without adequate separation, the culture and resources of the larger organization tend to crowd out those of the smaller start-up, such that the start-up’s strengths are lost.

Christensen mirrors this idea by recommending that a start-up or spin-off have autonomy so that it can explore innovations without influence from the parent company. He also implicitly acknowledges McKenna’s advice by pointing out the problems that established companies have adopting disruptive innovations: Most of these are not a problem for a small start-up, but if the start-up gets absorbed into the established company (or is never sufficiently separate from it) then the established company’s problems will still apply.

2. Adequate communication. While maintaining autonomy, the two organizations also need to communicate enough that they both have a clear understanding of who is responsible for what. McKenna warns that when organizations try to collaborate without adequate communication, important tasks are often left undone because each org assumes the other is taking care of it.

Christensen doesn’t address this, likely because he considered only collaboration between an acquired start-up or a spin-off organization, and doesn’t address collaboration between separate companies. We might infer that collaboration between separate companies more often fails due to inadequate communication, while collaboration between two organizations of the same parent company is more likely to fail due to inadequate separation.

Introduction: Disruptions Make Successful Companies Stumble

Innovations have the potential to upend industries. These kinds of significant innovations—called disruptive innovations—don’t come along very often, but when they do, they change how companies make and market products, the types of customers who buy the products, and how they use the products.

When disruptive technologies emerge, dominant, well-run companies often stumble. These companies tend to use the same sound business judgment that has guided them through previous changes, including:

- Listening to what current customers want

- Providing more and improved versions of what customers want

- Investing in projects that promise the highest returns

However, in the face of disruptive innovations, these strategies don’t produce the same results. This is the innovator’s dilemma: The approaches that lead to success in adopting most innovations lead to failure when confronting disruptive innovations.

This book provides insight for both innovators and established companies’ leaders on how to navigate disruptive innovations. The author takes on two key questions:

- Why do so many successful businesses fail when confronted with disruptive innovations in their industries?

- How can businesses succeed despite the unpredictability of disruptive innovation?

There’s no way to get around the uncertainty of innovation, but you can reduce the uncertainty by understanding the traits of disruptive innovations, effective strategies for adopting them, and how to tell the difference between a disruptive and non-disruptive innovation.

In Part 1, we’ll look at how and why successful, well-managed companies often fail when faced with disruptive technologies. In Part 2, we’ll cover strategies that established companies can use to avoid falling into these common traps, and how the companies can successfully adopt disruptive technologies.

The author was a Harvard Business School professor who developed the theory of disruptive innovation through extensive research, coupled with his experience as a former entrepreneur and management consultant. (Shortform note: This book was originally published during the 1990s tech boom, in which innumerable companies faced disruptions. The Economist named The Innovator’s Dilemma among the six most important business books ever written.)

(In the context of this book, “technology” means any process a company uses to produce its products and services, and “innovation” is anything that causes a technology to change.)

Part 1 | Chapter 1: Customers Discourage Disruptive Products

Typically companies succeed by giving customers what they want—if you keep your customers happy, your profits should stay high. But, as we’ll see, disruptive innovations don’t initially appeal to a company’s current customers.

Customers’ disinterest in disruptive technologies discourages established companies from investing in developing the disruptive products, which leads to the companies’ eventual downfalls. Those companies that fail to adopt the disruptive technologies get the rug pulled out from under them later, when they discover that the disruptive products are taking over their market because the technologies have improved enough to satisfy their customers.

We’ll look at the effect of customers’ influence in the disk drive industry, which experienced an exceptionally rapid pace of change in technological advancements and market structure.

Technology Mudslide Hypothesis in the Disk Drive Industry

Disk drives are responsible for reading and writing data on computers, using the binary system of 1s and 0s. IBM produced the first disk drive in the early 1950s. The drive was called RAMAC, which stood for Random Access Method for Accounting and Control.

Soon, other companies began producing disk drives. By 1976, there was about $1 billion in disk drive production.

Between 1976 and 1995, 129 startups entered the industry. During those two decades, each crop of entrant companies quickly graduated to become established firms, as new innovations disrupted the industry—and brought new generations of entrants—at an accelerated rate. Ultimately, all but 20 of the companies failed.

Some people blamed the high rate of failure on the rapid pace of technological advancement, which far exceeded most other industries. Based on this assumption, the author developed the technology mudslide hypothesis.

The technology mudslide hypothesis stated that keeping up with the breakneck pace of change was like working against a mudslide to climb a hill: It required every ounce of companies’ focus and effort, and pausing even for a minute would mean getting buried.

However, data ultimately debunked this theory. In reality, neither the complexity nor the pace of technological advancement led to companies’ failures—it was the type of technological change that determined companies’ fates. Specifically, established companies failed when confronted with disruptive innovations.

Sustaining vs. Disruptive Innovations

There are two types of technological innovations:

1) Sustaining innovations simply improve upon the performance of the industry’s existing products, thus catering to the established market. This represents the majority of technological advancements in any industry. Most companies that produce goods follow a fairly consistent trajectory of improving their products: They adopt technological advancements as they become available, and they release updated versions of their products with the new improvements.

Some sustaining innovations are simple changes, while others are technologically complex. Regardless, no matter how complicated the change, established companies almost always lead their industries in producing and marketing sustaining innovations.

2) Disruptive innovations disrupt the performance improvement trajectory. These technologies don’t appeal to existing customers—instead, they open up an entirely new market.

Disruptive innovations take many forms: Some are technologically advanced, while others are simple reconfigurations that offer new features. Some disruptive innovations invade markets like wildfire, while others take years or decades to take hold. No matter what the disruptive innovation is, entrant firms—or startups—almost always become the dominant forces in producing and selling it.

We’ll take a closer look at how these two types of changes impacted established and entrant firms in the disk drive industry. In the context of this book, established firms will refer to companies that existed before a given technological change, and entrant firms will refer to companies that started up at the same time the innovation was emerging.

Case Study: Disruptive Innovations in the Disk Drive Industry

There were only a handful of disruptive changes in the disk drive industry, but they caused established firms to crumble. The most significant of these changes was the shrinking of disk drives.

Two of the most important characteristics of disk drives are physical size and capacity. The industry was in a constant push to fit more data capacity on smaller drives.

In the 1970s, the high-capacity 14-inch drive was standard for mainframe computers, the huge machines used by large businesses for processing data and transactions. Between 1978 and 1980, entrant firms introduced a disruptive technology: a smaller, lower-capacity 8-inch drive.

The 8-inch drive didn’t have enough capacity for mainframes, but it was perfect for the emerging market of minicomputers—mid-sized servers used for business, scientific projects, and databases—which were a step down in size and power from mainframe computers.

At first, the 8-inch drives cost more per megabyte of capacity, even though the drive’s total price was lower than the 14-inch drive. The market tolerated the higher price-per-megabyte because it valued the drive’s smaller size.

Over time, 8-inch drive manufacturers improved capacity and reduced costs so much that the 8-inch drives eventually had a lower cost-per-megabyte than the 14-inch drives. Additionally, the 8-inch drives began invading the 14-inch drives’ market: The 8-inch drives’ capacity had increased enough to suit low-end mainframe computers, eventually pushing 14-inch drives out of the low-end mainframe market.

Among 14-inch drive manufacturers, two-thirds never entered the 8-inch drive market—and those that did were two years behind the 8-inch startups. Although the established firms that entered the 8-inch market had products that performed just as well, they couldn’t compete with the entrant firms. Eventually, every 14-inch drive manufacturer failed.

The 14-inch drive manufacturers hesitated or failed to enter the 8-inch market because their mainframe computer customers didn’t want smaller drives. Mainframe computer makers wanted more capacity at a lower cost-per-megabyte, and 8-inch drives couldn’t offer that—at first. Ultimately, listening to their customers led to the 14-inch firms’ demise.

This pattern repeated multiple times in the evolution of the ever-shrinking disk drives.

The 5.25-Inch Drive

When the entrant Seagate Technology created the 5.25-inch drive in 1980, it had a sixth of the megabyte capacity of 8-inch drives and five times the access time (the higher the access time, the slower the computing speed).

Minicomputer manufacturers weren’t interested in the innovation, so Seagate had to find another market. The company turned to the emerging market of personal desktop computers, where the drive’s inferior capacity was less important than its smaller size and lower total price.

As in the transition from 14- to 8-inch drives, the established 8-inch firms that eventually produced 5.25-inch drives were about two years behind entrant firms. And half of 8-inch makers never entered the 5.25-inch market and eventually failed.

As the capacity of the drives increased, they eventually became sufficient for minicomputer and mainframe manufacturers. Again, the disruptive innovation began in an emerging market and eventually invaded the established market.

The 3.5-Inch Drive

The 3.5-inch drive was created by a company called Rodime in 1984, but the technology took off when the firm Conner Peripherals brought it to market in 1987. Similar to previous evolutions, this drive was physically smaller and offered less capacity than existing products.

Conner found a market in new portable and laptop computers, which valued the drive’s smaller size, lighter weight, and decreased power needs.

Seagate—the innovator of the 5.25-inch disk drive, and now an established firm—could have beat Conner to the market, but the company fell into the trap of listening to its customers. In 1985, Seagate’s engineers introduced a 3.5-inch drive prototype to customers, but the desktop computer makers weren’t interested. Seagate’s executives killed the 3.5-inch project because they doubted that the smaller drives would bring in enough revenue to make it worth the investment.

However, after Conner began selling 3.5-inch drives, Seagate revived the project—but instead of targeting the emerging market of laptop manufacturers, Seagate sold the smaller drives to desktop computer makers. Although Seagate had hesitated to invest in the disruptive technology for fear of cannibalizing its existing sales, that’s exactly what happened when the company finally entered the market because it sold the drives to its existing customers.

Seagate’s mistake is a common misstep among companies facing disruptive technologies. To avoid this, established companies should adopt disruptive innovations soon after the technologies emerge, and the companies should target the disruptive products’ emerging markets, instead of trying to tailor them to existing markets.

The 2.5-Inch Drive

In 1989, an entrant firm called Prairietek introduced a 2.5-inch drive and dominated the market. But by the end of 1990, Conner Peripherals produced its own version of the drive and took 95 percent of the market.

In this case, the entrant Prairietek didn’t have the advantage over the established Conner Peripherals because the 2.5-inch drive was a sustaining—not a disruptive—technology. The smaller drive appealed to the same laptop makers that used 3.5-inch drives, so the innovation merely represented a technological improvement.

Throughout the decades of improving disk technology, each round of incumbents allowed themselves to be led astray by their customers’ input. In the next chapter, we’ll talk about why.

Exercise: Identifying Disruptions

Disruptive innovations are all around us. Recognizing them and their impact will help you deal with them in business.

What is one example of a disruptive innovation that has either affected the industry you work in or impacted your daily life?

How did the established market operate before the disruption?

What was the emerging market the disruptive technology initially targeted?

How has the disruptive innovation affected the established market?

Think of the top companies in that industry. Are they established or entrant companies?

Chapter 2: Value Networks

In order to explain why dominant companies often fail in the face of technological change, most experts offer two theories:

- The Organizational Structure Framework: Companies’ organizations, managements, or cultures can’t adapt to radical innovations that require different communication patterns and workflows.

- The Capabilities Viewpoint: Companies develop certain skills and knowledge from producing their existing products, and they stumble when a radically new technology requires a different set of skills and knowledge.

Although these theories help explain many firms’ failures, they don’t address what happened in the disk drive industry, where established firms adopted radically new technologies for various sustaining innovations, but they failed when faced with relatively simple innovations like the 8-inch drive. As we saw in Chapter 1, a major factor determining whether a company adapted to disruptive technologies was whether its customers were interested in the new technology.

A third theory—the theory of value networks—explains how customer input is part of a larger system that determines how companies respond to customer input, set and pursue goals, and react to industry changes, such as disruptive innovations.

Value Networks

Just about every product requires specific component parts—for example, a mainframe computer needs circuit boards, a central processing unit, and disk drives, among other things. Component parts, then, require their own component parts: Disk drives need disks, a motor, and a spindle. While some companies produce their own component parts, most buy them from various suppliers.

This creates a nested network of producers and markets. Each nested network represents a unique value network, because the chain of supply and the products being manufactured determine each component’s value.

There are two metrics that factor into a product’s value in its value network. Let’s look at them in terms of a disk drive in a network producing laptops versus a network producing mainframes:

- Performance attributes: These are the traits that customers value in a product. For laptop manufacturers, the most valued attributes for disk drives are small size, durability, and low power needs. By contrast, mainframe makers value speed, megabyte capacity, and reliability.

- Cost structure: This is determined by a product’s overhead costs, production volume, and price point, and it dictates the gross profit margins manufacturers need to meet. Laptops entail high production volume in low-cost factory settings and distribution to retailers, thus laptop makers need only 15-20 percent gross profit margins to cover overhead. By contrast, mainframes require low-volume, custom manufacturing; direct sales, requiring a sales team; and ongoing tech support for customers, which means mainframe makers need 50-60 percent gross profit margins to cover overhead.

A company’s value network provides the context for the organization’s decisions and actions, including how it approaches innovations. If an innovation affects a product’s attributes or cost in a way that is highly valued within the value network, then the company is more inclined to pursue it.

This framework illustrates why established firms are reluctant to allocate limited resources—including time, money, and personnel—to disruptive innovations, which have low value in both metrics:

- Disruptive innovations don’t have attributes that appeal to existing customers.

- Disruptive innovations promise low profits because they are initially marketable only to small, emerging markets.

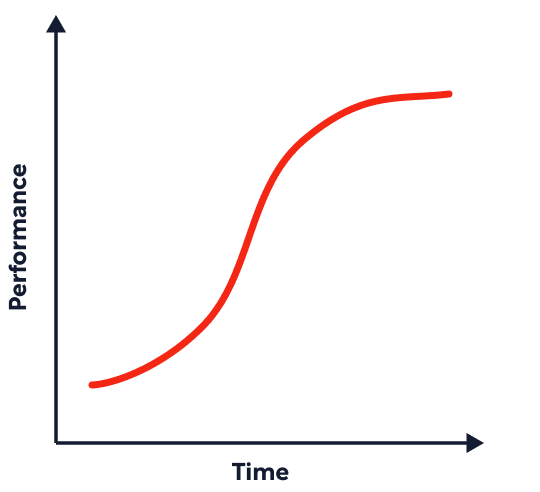

The Technology S-Curve Framework

Some businesses use the technology S-curve framework to determine when to adopt innovations—but the S-curve framework only applies to sustaining innovations that replace products within the same value network.

When a technology is first developed, progress is slow and the slope of the S-curve is gradual. Then, the slope steepens as improved understanding and engineering bring rapid progress. Finally, the slope nearly plateaus as technology has been improved and refined so much that progress slows significantly.

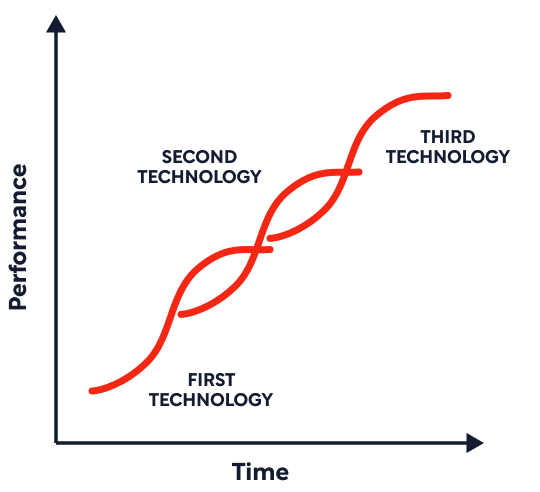

When a new sustaining technology emerges, the S-curves of the old and the new technologies overlap: The new technology is in the early acceleration stages while the old technology begins to plateau. The most successful companies transition from the old to the new technology at the moment that the two curves intersect, shown on the graph. The companies that do this best are the established firms.

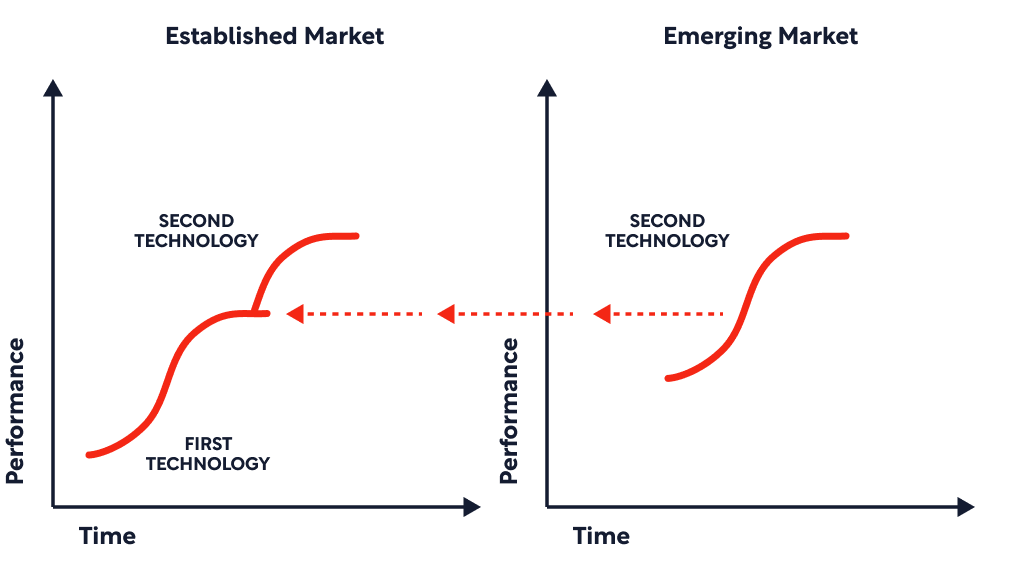

However, when a disruptive technology emerges, its S-curve is on an entirely different graph because, by definition, it serves a different market and exists in a different value network. At a certain point, once the disruptive technology’s performance has improved enough, it may invade the previously established market and replace the old technology, in which case it would look like these graphs.

Case Study: How Value Networks Influenced Seagate

Let’s look at how the 5.25-inch drive innovator Seagate’s value network influenced the company’s decision-making as it confronted the emergence of disruptive 3.5-inch disk drives. The development and spread of the disruptive technology breaks down into six steps:

Step 1: Established Firms Develop the Technology

Established companies often develop disruptive technologies first—though the projects are typically initiated by engineers, not company leaders—and entrants are simply at the forefront of bringing the technology to market.

Example: Seagate was actually among the first firms in the industry to develop 3.5-inch drives, although it wasn’t one of the first to market the drives. Seagate’s engineers had made dozens of prototypes of the 3.5-inch drives by the time company managers finally approved the project. When they got approval, the engineers showed their prototypes to the firm’s marketing team.

Step 2: Firms Gauge Customer Interest

When established firms consider developing a disruptive product, they gauge the existing market’s interest in the new technology. By definition, disruptions aren’t attractive to established customers, and the customers’ negative response typically dissuades companies from proceeding.

In some cases, executives allow disruptive projects to continue past this stage—but a lack of conviction about the product’s potential undercuts the commitment to the project. As a result, in day-to-day situations, time and resources are diverted to other projects.

Example: Seagate’s marketers showed the drives to customers, who weren’t interested in them because the low-capacity drives didn’t meet their needs. Based on customers’ feedback, the marketing team created dreary sales forecasts, and company leaders killed the project.

Step 3: Established Firms Double-Down on Sustaining Innovations

Based on customer input, established firms’ marketing teams not only discourage executives from pursuing disruptive technologies, but they also push for increased effort on sustaining technology to improve existing products.

Example: Seagate compared the market forecasts for 5.25-inch and 3.5-inch drives. The 5.25-inch models with 60-100 MB capacities were projected to bring in 35-40 percent gross profit margins. On the other hand, the 3.5-inch drives had an unknown profit projection—plus, the company’s existing 20 MB-capacity drives brought merely 25-30 percent gross margins. Using these comparisons, Seagate upped production of new-and-improved 5.25-inch models.

Step 4: Startups Form and Find Customers

After leadership at established firms turn away from disruptive projects, frustrated engineers often join entrant firms in pursuing the new technology. The startups face the same struggle as established firms in using the disruptive technology to attract customers in the existing market—but, unlike established firms, the entrants have no other products to fall back on, so they’re forced to find a market. Through trial and error, the startups eventually find the emerging markets for their innovations.

Example: Unhappy with managers’ strategies, employees from Seagate and Miniscribe—the two biggest 5.25-inch drive producers—left the established firms to found Conner Peripherals, which ultimately led the industry in 3.5-inch drives. Conner knew that desktop computer makers wouldn’t buy the 3.5-inch drives, so it hit upon the laptop market. The outlook for the laptop market was unclear, but the company had no choice but to try it.

Step 5: Disruptive Products Invade the Established Market

The disruptive technology’s performance improvement progresses up the S-curve until it reaches a level of sophistication that appeals to the customers that previously rejected it. In addition to dominating in the emerging market, the new technology then invades the old technology’s market.

Example: The capacity improvements for the 3.5-inch drives outpaced what the laptop market needed, and the small drive soon satisfied desktop makers’ needs. With the capacity increase, the 3.5-inch drive’s small size, lower price, and reliability made it more attractive to personal computer makers than the 5.25-inch drives.

Step 6: Established Firms Try to Catch Up

Once the startups begin invading the old technology’s market, established firms make an effort to defend their territory and revive the projects they’d killed in Step 3. However, the established firms discover that the entrants have a competitive advantage.

Since the entrants developed their disruptive products in a lower value network (the emerging market), they created cost structures that made the product profitable at lower gross margins. The entrants bring their lower cost structures to the established market, which allows them to offer lower prices than the established firms, whose organizations are built around higher cost structures.

Example: When Conner Peripherals began selling its 3.5-inch drives to desktop computer makers, Seagate dusted off its 3.5-inch prototypes. Since Seagate had waited until the disruptive 3.5-inch drives invaded the desktop industry before producing its own models, the company simply sold the smaller drives to its existing customers—cannibalizing its own 5.25-inch sales. Seagate never expanded into the laptop market.

Predicting Flash Memory’s Fate

Flash memory was developed in the 1980s and threatened to disrupt the disk drive industry. Initially, flash memory attracted customers outside the computer value network, including makers of heart monitors, cell phones, industrial robots, and modems. (Shortform note: Today, flash memory is ubiquitous and is used in solid-state hard drives, smartphones, USB flash drives, and digital cameras.)

True to any disruptive technology, flash memory had immediate advantages and disadvantages compared to disk drive technology. The advantages included:

- Less than 5 percent of the power consumption of a disk drive with the same capacity

- More durability in harsh conditions

The disadvantages included:

- Significantly higher cost-per-megabyte

- Shorter lifespan

The flash card market brought in $45 million in 1993 and $80 million in 1994—and that was projected to jump to $230 million by 1996.

Would flash memory invade the disk drive value network and upend established firms’ dominance? Here’s how each of the theories we discussed would guide predictions.

1) The Organizational Structure Framework would categorize flash memory as a radical technology. As such, established firms that were set up to facilitate a different workflow and communication structure than flash memory demanded could only develop flash memory products if they created independent entities to lead the effort.

This held true: Seagate bought a 25 percent equity in SunDisk Corporation (which was later renamed SanDisk) to design and develop the flash memory cards.

2) The Capabilities Viewpoint would recognize that, although flash memory used significantly different technology than disk drives, disk drive makers had all the knowledge they needed to succeed. Established firms were experienced in designing technology, buying component parts from suppliers, coordinating products’ assembly, and marketing and selling them. The companies could apply these general capabilities to producing flash memory and competing with startups.

Seagate did, in fact, use its capabilities to go into business with SunDisk, find component suppliers and a manufacturer, and then market the products itself.

3) The Technology S-Curve Framework would note that the rate of improvement of disk drive technology had not yet slowed to a point that the S-curve of the new technology’s progress could intersect with the old technology’s S-curve. That means that disk drives were not yet at risk of being replaced by flash memory.

4) The Value Network Framework would disregard established firms’ organizational structures and capabilities as reliable predictors of whether the firms would be toppled, and it would disregard the S-curve framework because that only applies to sustained technologies. Instead, the Value Network Framework would predict whether established firms would invest in their own flash memory products based on their customers’ interest.

By the mid-1990s, flash memory couldn’t offer computer makers what they needed, so Seagate pulled its few flash products from the market, though it retained its equity in SunDisk.

Outcome of Flash Memory Innovation

The Value Network Framework best predicted established companies’ trajectories in response to flash memory.

Disk drive makers hit a limit on how much they could lower the production cost per drive. Since low-capacity disk drives had the same cost floor as high-capacity drives, disk drive makers focused on producing high-capacity drives (around a gigabyte or more), which better served its customers.

This left an opening for flash memory cards to fill the void in the emerging 10-40 megabyte market. Industry experts predicted that a 40 MB flash card and 40 MB disk drive would be around the same price by the time the book was published in 1997.

(Shortform note: Flash memory eventually improved enough to invade an established market and replace hard disks in laptops. Flash-based solid-state drives (SSDs) are now in top-performing laptops, including the MacBook Pro and Microsoft Surface.

Although Seagate quickly withdrew its flash products from the market, the company made a wise decision in retaining a stake in SunDisk—in fact, it’s a strategy we’ll talk more about in Part 2. SunDisk was eventually renamed SanDisk, and the company is now one of the top eight vendors in the memory card market worldwide.)

Chapter 3: Case Study—The Excavator Industry

To illustrate that the principles and impacts of disruptive innovations are universal, now we’ll take a look at a very different industry: excavators. In contrast to the rapid changes that took hold in the disk drive industry, the disruptive technology we’ll be talking about—hydraulics to replace cable-operated actions—took 20 years to take over the excavator market.

Here’s an overview of the innovations that impacted excavators’ evolution:

- 1837-1920s: The steam shovel was invented. All mechanical earthmoving equipment was powered by steam.

- Early 1920s: Gasoline replaced steam. Gasoline-powered equipment was more powerful, reliable, and affordable than almost any steam shovel, with the exception of the biggest ones. Despite the major technological shift, this was a sustaining innovation because it served the same market—just with improved performance—and 23 out of the 25 biggest steam shovel manufacturers successfully switched to gas excavator production.

- Late 1920s to 1940s: Several other sustaining innovations followed, including diesel power, electric motors, and a design change that gave the excavators increased reach and flexibility.

- 1940s to late 1960s: A disruptive technology emerged—excavators that used hydraulics instead of cables to move the arms and bucket.

When hydraulic excavators hit the industry, they eventually wiped out nearly all the established manufacturers. In the 1950s, there were about 30 established excavator companies. By the 1970s, only four established companies had successfully transitioned to hydraulic excavators, and the industry was led by entrant firms (including companies that are still well-known, such as John Deere and Caterpillar).

Finding an Emerging Market

During the reign of cable excavators, there were three markets:

- General excavation (digging holes for things like basements or canals)

- Sewer and piping (digging long trenches)

- Open pit and strip mining

Each market had unique needs—for example, sewer and piping customers needed narrower buckets to dig trenches, while mining customers needed larger bucket capacity to move dirt efficiently. But overall, cable excavators’ most highly valued performance characteristics were:

- Reach (how far the arm and bucket could extend)

- Bucket capacity (cubic yards of dirt per scoop)

When hydraulic excavators were first developed, they had a fraction of the bucket capacity and reach of cable excavators—insufficient for the needs of any of the cable excavator customers. Hydraulic entrant firms had to find another market, so they adjusted the machines to be mounted on tractors, and they called them backhoes.

Backhoes became the perfect solution for smaller, residential construction jobs. Contractors on these projects previously had to hand-dig narrow ditches for sewer lines, because the job sites and project budgets were too small to bring in full-sized cable excavators. Hydraulic excavators opened the residential construction market to using excavators for the first time, because they offered attributes that cable excavators couldn’t, including:

- Smaller size

- More affordable price

- Narrow buckets that were ideal for digging residential sewer trenches

- Tractor mounts that made them faster and more mobile than traditional excavators on tracks

Not only had hydraulic excavator makers found their market, but they struck it while tract housing construction was booming following World War II and the Korean War.

An Established Firm’s Failed Attempt to Adopt Hydraulics

In 1950, a dominant cable excavator manufacturer, Bucyrus Erie, saw hydraulic excavators’ rise and bought a small hydraulic backhoe company. But instead of entering the emerging residential construction market, Bucyrus created a hydraulic-cable hybrid to market to its existing customers.

The machine, called the Hydrohoe, used hydraulics to guide the shovel into and through the dirt, but it used cables to lift the bucket. The cables enabled the Hydrohoe to lift bigger loads, which Bucyrus thought would make the machine robust enough for its customers. However, the Hydrohoe still didn’t have enough capacity or reach for Bucyrus’s customers, so the product languished on the market for 10 years and the company eventually resumed selling cable excavators.

Hydraulic Excavators Invade the Established Market

Over time, backhoes improved and significantly increased bucket capacity—from ⅜ cubic yard in 1955 to 10 cubic yards in 1974. With improved capacity, hydraulic backhoes ascended into the traditional cable excavator market.

Once hydraulic excavators improved enough to satisfy cable excavators’ customers, the performance attributes that customers valued began to shift. Put another way, now that both models were good enough to get the job done, increased capacity was no longer a competitive advantage.

With their capacity needs satisfied, customers started making buying decisions based on reliability instead of capacity. (We’ll talk more about this concept in Chapter 9.) Hydraulic excavators didn’t carry the risk of having a cable snap while carrying a heavy load, so they began to pull ahead of cable excavators.

At this point, established firms’ businesses started to take a hit. Some firms adapted by developing hybrids like the Hydrohoe, but all of them treated hydraulic technology as a sustaining innovation that could improve their products to market to their existing customers. All but four of the companies ultimately failed.

By contrast, the entrant companies had framed hydraulics as a disruptive technology and targeted an emerging market. In other words, the entrants found a market to match the technology, while the established firms tried to adapt the technology to meet their market. Even though the disruptive technology eventually entered the traditional market, the entrants had certain advantages because they started in the emerging market and expanded upmarket.

During the two decades that the startups were serving the emerging market, the companies developed expertise in designing, improving, and selling the products. By the time they entered the traditional excavator market, that experience gave them an advantage over the established firms.

Excavator Companies Listened to Their Customers—And It Cost Them

Cable excavator manufacturers didn’t fail because hydraulic technology exceeded their capabilities or because they were oblivious about their customers’ needs. Rather, the companies failed because they were tuned into their customers’ needs, and hydraulic excavators didn’t make sense for their customers—and, thus, for their profits. The established companies had to focus their resources on staying competitive in their market.

Ironically, these decisions based on the companies’ survival cost many firms their entire businesses. In the next chapter, we’ll talk about how an organization’s past success creates barriers to adopting disruptive innovations.

Chapter 4: Upward Mobility and Downward Immobility

Successful companies typically focus on growing and moving upmarket with higher-priced products, higher-tier customers, and larger profits. However, this upward mobility makes firms downwardly immobile—it impedes them from adopting disruptive innovations, which always start downmarket.

Barriers to Downward Mobility

Established companies face three key barriers to downward mobility:

- Cost structures that favor seeking higher profit margins upmarket over cutting costs to remain profitable downmarket

- Organizational cultures that pull efforts toward upmarket projects

- The upmarket drift of a company’s customers and competitors

Barrier #1: Cost Structure

As discussed in Chapter 2, organizations develop cost structures that fit their value networks—value networks for higher-priced products require larger gross profit margins to cover higher overhead costs than value networks for lower-priced goods. These cost structures force companies to maintain profit margins to simply stay afloat.

In fact, most companies aim to move to progressively higher-value markets. This is especially true when disruptive technologies invade their markets, because the disruptive products generally enter the low end of the market and gradually climb to higher tiers. For example, when 3.5-inch disk drives ascended from the laptop to the desktop market, Seagate didn’t try to compete—instead, the company increased efforts to improve 5.25-inch drives enough to enter the market for minicomputers.

If an established company wants to invest its limited resources in the small, low-profit market for a disruptive product, company leaders would have to find a way to somehow cut costs. However, a company’s overhead costs include market research, product development, and marketing that’s critical to remaining competitive in its existing market. Most companies find it impossible to bring in enough profits from existing products while also trimming overhead enough to invest in disruptive ones.

Barrier #2: Organizational Culture

A company’s upward or downward mobility is determined by the projects it chooses to invest in, and most companies have processes that steer them toward high-profit projects. Although it may appear that senior managers are responsible for choosing the projects that a company invests in, middle managers actually play a more significant role in this process as gatekeepers.

Middle managers filter the ideas that come from engineers and other employees, carefully deciding which projects they’ll pitch to senior managers. Middle managers want to pitch only projects with a high likelihood of success and profitability—otherwise, they risk taking a hit to their credibilities and careers—and upmarket projects are the surest way to achieve that.

Under normal circumstances, a company’s success depends on having processes like this (formal or de facto) that weed out low-profit projects—otherwise, the company would waste too many resources on projects that don’t provide a return on investment. But these same processes steer companies away from disruptive technologies, making the firms vulnerable to being overtaken by the disruption.

Barrier #3: Upmarket Drift

Often, companies can drift upmarket without making a conscious effort to ascend to the next value network. Companies drift upmarket when their customers are pursuing higher markets, and when their competitors are similarly leaning upmarket to meet customers’ needs.

As companies move upmarket, they create openings in lower value networks for entrants to move in with disruptive products. Let’s look at how this played out in the steel industry.

Case Study: Minimills Disrupted the Steel Industry

In the mid-1960s, steel minimills disrupted the steel industry. As the name suggests, the minimills were simply steel mills at a much smaller scale.

When they emerged, the minimills could only produce lower-quality, lower-cost steel products than the established firms, the integrated steel mills. The only product they could make with the lower-quality steel was reinforcing bars (rebars), which were used to strengthen concrete.

Rebars represented the lowest quality, cost, and profits of any steel products. Additionally, rebar customers were less loyal to manufacturers than customers of any other steel products, because price mattered more than any other attribute. As a result, integrated steel mills didn’t miss the rebar customers that the minimills took from them.

Over time, minimills increased the quality of their steel and invested in equipment to make different products. Minimills subsequently took over the next two highest markets:

- Larger bars, rods, and angle irons

- Structural beams

Paradoxically, integrated steel mills’ profits grew at the same time they were being pushed out of these low markets. Ceding the lowest-profit products to the minimills allowed the integrated mills to invest in high-quality steel products, such as rolled sheet steel, that brought in the biggest profits. As a bonus, the rolled sheet steel market was insulated from minimills’ threat because minimills couldn’t afford the equipment needed to make high-quality sheet steel—but that wouldn’t be true for long.

Thin-Slab Casting Causes Another Disruption

In 1987, the steel industry was disrupted again by a new technology called continuous thin-slab casting, which opened the sheet steel market to minimills. The technology offered a much more efficient way of producing sheet steel at a significantly lower cost than traditional methods, and it made it feasible for minimills to begin producing sheet steel.

However, the quality of thin-slab cast sheet steel was initially too low to appeal to high-end customers, such as car, can, and appliance makers. The steel was only suitable for the low end of the market, for products such as corrugated steel and pipes. Since thin-slab sheet steel would only attract limited customers—and bring in low profits—integrated steel mills didn’t adopt the technology, instead investing in equipment to further improve the quality of their sheet steel for their high-end customers.

Unrestrained by high-end customers and higher cost structures, a minimill called Nucor was the first to adopt the thin-slab casting technology. Within seven years of opening its first thin-slab facility, Nucor had opened a second mill and controlled 7 percent of the sheet steel market in North America.

With time, the technology improved and raised the quality of the sheet steel. (Shortform note:

Eventually, thin-slab casting could produce quality that traditional thick-slab casters couldn’t achieve. By 2017, only nine integrated steel mills were still operating in the U.S., and they produced about one-third of the country’s steel. By contrast, there were more than 100 minimills that produced nearly two-thirds of the country’s steel.)

Part 2 | Chapter 5: Overcoming Resource Dependence

Now that we’ve outlined the factors that cause established firms to fail when confronting disruptive innovations, we’ll talk about how managers can avoid falling into these traps.

Established firms generally struggle to survive disruptive innovations, but if managers understand the governing principles of disruptive technologies, they can weather the storm or, at best, harness them for their success. Companies that don’t know what they’re up against or how to navigate it will almost surely succumb to disruptive technology’s takeover.

Consider this analogy: When humans first attempted to fly, they attached wings to their arms, jumped off of tall objects, and flapped as hard as they could. They soon discovered that the methods that worked for birds didn’t work for humans. However, when they learned about the forces at work—such as gravity and the concepts of drag, lift, and resistance—they were able to harness these principles and eventually take flight.

Through the next five chapters, we’ll explore each of the five principles of disruptive technology, illustrate how they create problems for established companies, and offer solutions to navigating them. The five principles are:

- Customers and investors dictate a company’s resources.

- Small markets can’t keep big companies alive.

- Companies can’t rely on market research for unknown and emerging markets.

- A company’s capabilities in one context are its disabilities in another.

- Customers don’t always want the newest technological advance.

We’ll start by discussing Principle #1 and talking about a few case studies that illustrate how this principle played out in several industries.

Principle #1: Customers and Investors Dictate a Company’s Resources

Although company leaders appear to be in control of an organization’s decisions and direction, the theory of resource dependence states that customers and investors are the primary deciders of a company’s actions. This is because customers and investors provide the resources the company needs to stay in business, so everything the organization does essentially is in an effort to keep them happy.

Problem: Resource Dependence Impedes Disruptive Innovation

Generally, the strategy of satisfying customers and investors is not only effective but also essential to a company’s survival. However, as we talked about, disruptive technologies are inherently unappealing to current customers, and the low profits they offer are also unattractive to investors. Consequently, this approach causes established firms to neglect disruptive innovations until they’ve improved enough to be attractive to current customers—and by then, it’s too late.

The culture that grows out of resource dependence impacts everyone in the company: From the senior managers down to the most junior employees, everyone knows what kinds of work is good for the company and for their personal careers.

Even if a manager decides to take a chance and pursue a disruptive innovation, everyone working on the project needs to believe in it in order for it to be successful. If team members don’t believe in the disruptive project, they make innumerable small day-to-day decisions—such as prioritizing their time toward other assignments—that’ll ultimately starve the project of the effort and attention it needs to succeed.

Solution: Create an Independent Organization

Rather than trying to convince employees to back a project, company leaders can create an independent entity—preferably in a separate physical location—to lead the development and marketing of the disruptive product.

The parent company’s culture and organization are built to succeed in its existing market, but the independent organization needs the separation to be able to develop the culture and cost structure that fit the disruptive innovation.

Principle #1 in the Disk Drive Industry

Let’s look at how three disk drive companies successfully handled Principle #1 when faced with disruptive innovations.

Quantum Corporation Financed Former Employees’ Startup

In the early 1980s, Quantum Corporation was a dominant manufacturer of 8-inch disk drives, which were used in minicomputers. When 5.25-inch drives disrupted the market, the company was nearly four years late to market its own 5.25-inch product.

When Quantum employees saw the next disruption coming, they didn’t want to be behind the curve yet again. The employees left Quantum and formed their own startup to make and sell 3.5-inch drives.

Quantum saw an opportunity: Instead of merely letting the employees walk away, Quantum financed and held 80 percent ownership of the startup, called Plus Development Corporation.

Besides the financial ties, Plus Development was completely independent—from its locations to its executives. The firm had a lot of success, which was a lifesaver to Quantum as the sales of its 8-inch and 5.25-inch drives dissipated over time.

After several years, Quantum bought out Plus Development and basically turned the startup into its main operation. As time went on, Quantum successfully adopted subsequent sustaining technologies and, by 1994, was the largest unit-volume disk drive manufacturer in the world.

Control Data Corporation Relocated Its Disruptive Product Team

Control Data Corporation (CDC) was an industry leader in 14-inch drive production for more than 15 years. When 8-inch drives entered the market, CDC was three years late in producing them—and the 8-inch drives it sold were almost entirely to existing customers.

CDC failed to capitalize on the potential of 8-inch technology and its emerging market because the project didn’t get the time and attention it needed. Instead, the marketers and engineers assigned to the project kept getting pulled away to work on new 14-inch models.

But when 5.25-inch drives arose, CDC took a different approach: The company sent the team assigned to work on 5.25-inch products to a facility in Oklahoma City—far from the company’s primary Minneapolis location. The physical distance allowed the team to put their entire focus on the 5.25-inch project.

CDC’s strategy worked. Although the company was two years behind the industry in introducing its 5.25-inch models, CDC held a decent market share and made a profit off the venture.

Micropolis’ CEO Fought to Launch the Disruptive Product Within the Company

Micropolis was a dominant 8-inch disk drive maker that managed to adopt disruptive 5.25-inch technology without creating a separate entity to lead the effort—but it wasn’t easy.

Micropolis’s CEO put his best engineers on the disruptive project and spent a year and a half fighting against the company’s organizational structure, which was designed to serve its customers in the 8-inch market. The CEO had to put all of his time and attention on the project to ensure that resources weren’t being pulled away.

The effort paid off, and Micropolis successfully transitioned from 8-inch to 5.25-inch drives. To do so, the company had to abandon all of its 8-inch customers—who initially had no use for the 5.25-inch models—and scramble to find 5.25-inch customers to replace the lost profits.

Principle #1 in the Personal Computer Industry

The evolution of disruptive technologies in the computer industry runs parallel to the evolution of disk drive technology, on which computers relied. Established mainframe computer makers were disrupted by the emergence of the minicomputer, which was disrupted by the personal computer, which was disrupted by the laptop.

Two minicomputer makers—Digital Equipment (DEC) and IBM—illustrate two starkly different approaches to confronting the disruptive innovation of personal computers.

DEC marketed personal computer lines four different times between 1983 and 1995, but each time they failed. During each attempt, the company led the personal computer project within its main organization. The problem was that DEC’s established cost structure and value network were incompatible with the value network it needed to enter to be successful in the personal computer market.

By contrast, IBM was successful in its personal computer venture. When IBM launched its personal computer project, it created an independent entity located in Florida, while the company’s main headquarters was in New York. The entity was empowered to take its own approach to creating a cost structure, sourcing component parts, and selling the products, independent of IBM’s main operations.

Principle #1 in the Discount Retail Industry

When discount retail stores began popping up in the 1950s, they caused a huge disruption for department and variety stores by selling nationally known brands at significantly lower prices.

Whereas department and variety stores sold products at about 40 percent of the wholesale price and turned over their inventory four times a year, discount retailers achieved the same profits by marking up the products only 20 percent and turning over inventory eight times a year.

Initially, discount stores sold low-end goods like hardware and small appliances to low-profit customers—namely, blue-collar wives with young kids. However, over time, the discount retailers began offering higher-end goods, such as clothes and home goods.

The two biggest variety store chains in the world—S.S. Kresge and W.F. Woolworth—took significantly different approaches to opening discount stores. The companies’ drastically different outcomes were yet more evidence that one organization can’t sustain two cost structures and cultures.

Kresge made a full transition from variety to discount stores. The company brought on a new CEO, hired a new management team, and steadily closed its existing stores. Through its full commitment to the disruptive innovation, Kresge found success. Its discount stores were called Kmart, and, 10 years after opening, Kmart’s sales were near $3.5 billion.

Woolworth tried to sustain its existing stores while also building its chain of discount stores, Woolco. The same set of managers were tasked with both projects, and the company continued opening new Woolworths at the same rate after opening Woolco as it had before. Ten years after opening, Woolco’s sales were about $0.9 billion. Another 10 years later, the last existing Woolco closed.

Principle #1 in the Ink-Jet Printing Industry

When ink-jet printing was introduced, it disrupted the laser-jet printing market. Although the new printers had lower resolution and higher cost-per-page, they were also smaller and cheaper per unit than the larger, higher-quality laser-jets.

Hewlett-Packard created a new entity and put it in Washington state to create physical and organizational separation from its main business in Idaho. HP executives even allowed the primary and the disruptive businesses to compete against each other in the market. This benefitted HP in multiple ways:

- It continued to earn laser-jet profits while the technology was dominant in its value market.

- It successfully commercialized the disruptive innovation and brought in profits from its ink-jet organization.

- If laser-jet sales declined with improvements in ink-jet capabilities, HP’s strong presence in the ink-jet market would help the company keep its former laser-jet customers.

Although one of HP’s businesses could end up killing the other, the company positioned itself in the best way to ride the transition from old to new technology.

Exercise: Navigating a Disruption

How would you lead your company through a disruptive innovation?

Imagine you’re the leader of an established company and a new innovation is emerging in your industry that threatens your current business. First, how would you determine whether or not it’s disruptive?

Now imagine that you’ve determined that the innovation is disruptive, and you decide that you want to spin-out an independent entity dedicated to the innovation. How do you make the case for investing in a risky, uncertain venture to your skeptical board of directors?

How involved would you be in the independent organization?

How would you ensure the entity was truly independent from the main organization (for example, staffing a dedicated team or putting the operation in a different physical location)?