1-Page Summary

We feel like we must choose between our money and our lives, so we spend time at jobs we dislike to earn money that we don’t have enough time or energy to enjoy. In other words, most of us choose money.

But we don’t need to choose; we can have both. This book offers 9 steps to transform your relationship with money and become financially independent—the state of not having to work for money.

How quickly you reach financial independence depends on your life circumstances, plus the speed and consistency with which you apply these steps.

Step 1: Understanding the Flow of Money in Your Life

To begin transforming your relationship with money, you need to understand the reasons you choose money, and why they’re harmful.

Problem #1: Choosing Money Over Life Hurts Our Wellbeing

We choose to stay in jobs we don’t like, even when it’s harmful to our wellbeing. The more time we spend working, the less time we have to care for ourselves and our families, be involved in communities, rest, and engage in other pleasures. This causes mental and physical stress, yet we have little to show for this sacrifice. People in the US are working more hours, saving less, and taking on debt.

The two main reasons that we choose work over wellbeing are:

- We don’t know how to leave jobs we don’t like.

- We don’t know how much money is “enough” for our happiness.

Problem #2: Choosing Money Over Life Hurts the Earth

We often consume things we want, but don’t need. When we over-consume, we deplete the planet’s finite resources, robbing future generations.

This modern consumer culture dates back to the early 20th century, when factories could produce more goods than ever before. But though more goods were available, people weren’t buying them because they didn’t need them. Companies needed a way to convince people to buy goods they didn’t need. Thus, the marketing industry was born.

To break this habit, we must break from the myths that drive consumer culture:

- Myth #1: Growth is good. We think that spending money will grow the economy, which will alleviate poverty, decrease unemployment, and improve the standard of living for everyone. But we can’t endlessly consume or we’ll deplete the planet of its finite resources.

- Myth #2: Technology will save us. We think the right technology will solve the world’s problems, and feel powerless as individuals to effect real change.

- Myth #3: The danger isn’t so immediate. We don’t feel the urgency to reduce consumption and take action to help the planet because climate change feels like a far-off apocalypse we won’t live to see.

Practice Step 1: Visualize Earnings and Calculate Net Worth

Now that you understand the dangers of choosing money over life, you can start the process of changing your relationship with money and living a life you love. The first step is to examine all the money that you’ve ever earned, and what you have to show for it.

This step has two parts:

- Calculate how much money you’ve earned in your lifetime. Look to sources like income tax returns, Social Security administration statements, and bank accounts.

- Calculate your net worth. Assign a value to each of your possessions worth more than a dollar. Sort them into things you own and things you owe—your assets and liabilities. Subtract your assets from your liabilities to calculate net worth.

Step 2: Tracking Your Money

To understand your relationship with money, you need a definition of money that is consistently true. With this definition, you’ll learn what it means to become financially independent, calculate your real hourly wage, and track your expenses.

Money and Financial Independence

People’s definitions of money vary. Some think of it as a material (such as the paper cash is printed on), or a reflection of human psychology—how you spend money reflects your personality. But the one consistently applicable definition is that it’s your life energy: Money represents the time and energy you dedicate to paid work.

With this definition, it’s easier to resist buying things you don’t need—what you buy must be worth the life energy you exerted to pay for it. Do you use and enjoy that jet ski enough to make it worth the life energy you paid for it? In the long-run, you’ll use the definition to transform how you spend both your time and your money to reach financial independence—when you’ve saved and invested enough money that you no longer have to work for pay.

Practice Step 2: Calculate Your Real Hourly Wage and Track Money

Step 2 has two parts:

- Calculate your real hourly wage. Examine the hours you spend working and doing work-related activities—getting ready for work, commuting, shopping for work clothes—per week. This step can help you evaluate whether a job you’re doing is worth the time and money you dedicate to it.

- Track money, down to the penny, that you receive or spend. You’ll use this information to start evaluating and reducing your expenses in Steps 3-6.

Step 3: Creating a Monthly Tabulation

In this step, you’ll categorize your monthly expenses to capture your unique spending habits. You’ll learn where your money goes and what you have to show for it.

This is different from making a budget. You’re not designating how much to spend in each category and subcategory. Instead, you’ll see what you spend and evaluate if your purchases are worth it.

Practice Step 3: Categorize Monthly Spending

- Develop categories and subcategories for your expenses. Include categories like Food, Housing, and Transportation. For example, in your housing category, create subcategories such as rent and utilities.

- Create a spreadsheet, budgeting tool, or Google Sheet to list different categories and subcategories. Then, sort each expense for the past month into your subcategories. For each subcategory and category, calculate the amount of life energy you spent by dividing the total by your real hourly wage.

- Calculate your savings for the month: (Income - Expenses) +/- total error. Error is any unaccounted money gained or lost for the month.

Step 4: Aligning Spending With Your Values, Purpose, and Dreams

To assess whether you’re living the life you want, you need to explore your values, purpose, and dreams. You’ll use this as the basis for Step 4: deciding whether your spending aligns with these benchmarks.

Values, Purpose, and Dreams

Our values, purpose, and dreams should dictate how we spend our time and life energy, or money. We feel fulfilled when our behavior is in line with these criteria. But this isn’t always the case, hence why people stay in jobs they dislike.

In order to align your time and spending with these criteria, you need to identify and get acquainted with your values, purpose and dreams. To do this, think about the fulfilling ways you spend your life energy. Fulfillment is a deep sense of satisfaction, contentment, or happiness that you get from working toward and recognizing achievements. We’ll explore some questions to help you define each of these things for yourself.

Practice Step 4: Evaluate Monthly Spending

Using your monthly tabulation from Step 3, ask the following questions for each subcategory and category of spending:

- Is the amount of happiness and contentment I got from these purchases worth the life energy I spent?

- Is spending this amount of life energy consistent with my values and purpose?

- If I didn’t have to work for money, would I spend more, less, or the same life energy on these purchases?

For each question, assign a value:

- Use a “-” if you didn’t get fulfillment proportional to what you spent and should spend less

- Use a “+” if you got fulfillment proportional to what you spent and think you should spend more

- Use a “0” if you got fulfillment proportional to what you spent and think your spending should stay the same.

Step 5: Graphing Your Income and Expenses

Now that you’ve evaluated your monthly expenses, you’ll learn how to track them and your income with a hand-drawn or digital graph. This graph will track your progress toward financial independence.

Seeing your spending and income in visual form will encourage you to:

- Earn more than you spend.

- Pay off your debt.

- Build savings.

Practice Step 5: Graph Your Income and Expenses

- Select an 18 by 12-inch or 36 by 24-inch piece of lined graph paper.

- Draw a horizontal (x) axis and mark time out in months.

- Draw a vertical (y) axis, mark out dollars.

- Each month, plot your monthly income and expenses (soon, you’ll add a line for investment income, too).

Step 6: Strategies and Categories to Cut Spending

To reduce your spending, you need to learn what it means to be frugal. Then, you can employ some strategies to help you spend less.

The True Meaning of Frugality

People think frugality means severely restricting your spending. But it’s really about enjoying things, whether you spend money on them or not.

To enjoy things more, you need to cultivate a high joy-to-things ratio—feeling great joy with each thing you buy or use. You’ll buy less because you feel more fulfilled with each purchase.

Practice Step 6: Reduce Spending

Use these 9 general strategies to reduce spending:

- Avoid shopping. Don’t go shopping when you don’t have anything you plan to buy.

- Spend only what you can comfortably afford. If you want to buy something, but don’t have enough money, wait to buy until you do.

- Repair your possessions. Repair things instead of replacing them with new ones.

- Use stuff to the end. This helps avoid frequent spending on the same items.

- Dive into DIY. Learning how to repair and fix things can save you money.

- Think about what you need. Create a list of things you anticipate needing to buy in the coming year.

- Investigate durability and multipurpose uses. Know whether a product will last long enough to make its price worth it.

- Don’t pay full price. Search for the best price, haggle, buy used, or get stuff for free.

- Devise new ways to meet your needs. Listen to your needs and desires and ask if they can be met without spending money.

Trim spending from the following 11 categories:

- Banking and Loans

- Housing.

- Transportation

- Health Care

- Sharing Your Skills (developing one or more you can provide in exchange for another service, like yard work or haircutting)

- Food

- Entertainment, News, and Cellphones

- Vacations

- Insurance

- Spending on Children

- Gift Giving

Step 7: Increasing Your Income

The more money you earn, the faster you’ll reach financial independence. Plus, if you earn more, you have more time for the activities that matter to you, so striving to maximize your income is in your best interest.

Just like with money, you need a better definition of work. Work is any activity that aligns with your values, purpose, and dreams, regardless of pay. With this definition, you’ll realign your time to earn money and do the work or activities you enjoy, even if they’re unpaid. In other words, your job doesn’t need to be your favorite activity, but it should pay you enough that you have time to do things you care about.

Practice Step 7: Increase Income

Here are ways to ensure you’re earning as much as possible for the life energy you invest in work:

- Ask for a raise. Get paid more for the work you already do.

- Ask for increased vacation time. Use time off to relax and do activities you enjoy.

- Ask to work fewer hours. If you’re earning more money than you need, you can work fewer hours and still meet your needs.

- Find another job or jobs that will pay you more for fewer hours.

Step 8: Graphing Your Investment Income

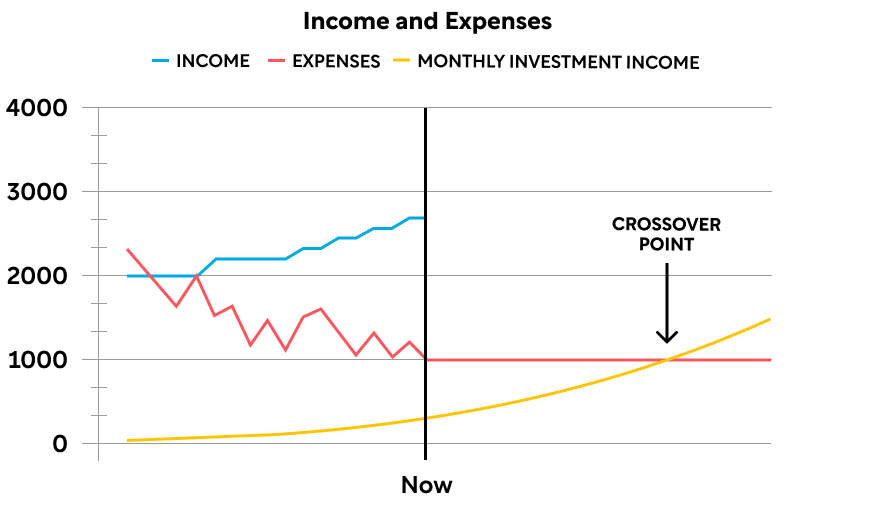

To learn when you’ll reach financial independence, chart when you’ll reach your crossover point—when your monthly income exceeds your monthly expenses—and you no longer need to work for money. Use your graph from Step 5.

Practice Step 8: Graph Your Investment Income

1. Calculate your monthly investment income and plot the figure on your graph. Use the formula monthly investment income = capital x current long-term interest rate divided by 12.

For current long-term interest rate, use the interest rate for 30-year US Treasury Bonds, or the interest rate for certificates of deposit.

This isn’t how much investment income you have at the moment you calculate it. It’s a projection of what monthly investment income you can expect if you invest your capital, regardless of the method you use to invest. For example, if you have $1,000 in capital and the current interest rate is 4%, the formula would be: monthly investment income = $1,000 x 4 % divided by 12, or $3.33 per month.

2. Apply this formula to your total savings each month and plot it on your graph. Eventually, you’ll be able to project approximately when you’ll cross over.

Step 9: Investing Your Capital

Learn where to invest your capital—savings that you don’t intend to spend.

This is the culmination of the program—having enough money coming into your life through passive income that paid employment is optional. It’s not about getting huge amounts of money but about knowing how to invest so that you have enough money for the remainder of your life.

Investing Lingo

Here are some key investing terms:

- Asset Classes: Different categories of investments, like stocks or real estate

- Passive Income: Also called investment income—money you don’t work to earn

- Risk Tolerance: Your willingness to make risky investments

- Time Horizon: How soon you plan to use money you’ve invested

Step 9: Choose Investment Options

Treasury bonds used to have the best interest rates of almost any investment, but this is no longer true. Now, it’s better to opt for a diverse investment portfolio that mixes low-cost index funds, certificates of deposit, real estate, as well as bonds. Considering your risk tolerance and time horizon, develop a plan to invest in a diverse mix of these assets. Do research and consult with a financial advisor if desired.

Introduction

Most of us feel forced to choose between “money” and “life,” and we inevitably choose money, sacrificing our relationships, health, and joy in the process. Instead of living our lives, we spend all our time at jobs we don’t really like to make money we have little time or energy to enjoy.

But we don’t have to choose between our lives and our money. We can have both. Your Money or Your Life offers 9 steps toward rethinking your relationship with money and becoming financially independent (FI), the state of not having to work for money. It’s the key to having both the life you want and the money to achieve and maintain it.

The 9 steps, in brief, are:

- Visualize earnings and calculate net worth.

- Calculate your real hourly wage and track money.

- Categorize monthly spending.

- Evaluate monthly spending.

- Graph your income and expenses.

- Reduce spending.

- Increase income.

- Graph investment income.

- Choose investment options.

FI-Thinking

To reach financial independence, you need to practice FI-thinking: cultivating a sense of curiosity toward money. There are 4 aspects to FI-thinking:

- Financial Intelligence: Looking objectively at your money. This includes the money you’ve earned and what you’ve bought with it. Plus, you need to know what money is, examine the money that comes into and out of your life, and evaluate whether the type of work you do and the time you spend doing it are in line with your values, purpose, and dreams.

- Financial Integrity: Understanding the effects of earning and spending money on yourself and the earth. You have to find the sweet spot—enough material goods to fulfill and enrich your life, but not so many that they become excessive or create clutter.

- Financial Independence: Escaping your dependence on money. This includes paying down debt and changing harmful assumptions you have about finances.

- Financial Interdependence: Recognizing the ways that you dedicate your time to the world and how that enriches your life.

You’ll practice each of these components as you work through the program’s 9 steps.

Reaching Financial Independence

When you’ll reach financial independence depends on the speed and consistency with which you apply the book’s steps. People generally fall into two categories:

- Hares apply principles quickly and set early financial independence goals.

- Turtles apply principles more slowly, but systematically to pay down debt and save money so that they’ll reach financial independence around retirement age.

Aside from how fast or slow you work through the steps, there are 3 styles of personal finance management:

- Ninjas work diligently to optimize their finances and investments through reading finance blogs, playing with their investment portfolio, and maximizing savings on purchases.

- Minimalists prioritize experiences over material goods and keep their lives clutter-free.

- DIYers, or do-it-yourself-ers, are “conscious materialists”: They make careful use of material resources and enjoy hands-on experiences with the world, like using wood scraps to build a birdhouse.

You may not identify with any of these styles, but it’s helpful to know how others apply the steps in this book. The bottom line: People will approach this book differently, but they all have a desire to change their relationship with money and work steadily to complete each of the steps.

Step 1: Understanding the Flow of Money in Your Life

There are a variety of factors that compel us to choose money over our lives. This chapter delves into the emotional factors and economic realities that dictate our relationship with work and money, as well as why choosing money over life is harmful to both our wellbeing and that of the planet.

Finally, we will explore the first step in reframing your relationship with money: visualizing your earnings and calculating net worth.

Problem #1: Choosing Money Over Life Hurts Our Wellbeing

There’s growing evidence that wanting more and valuing our job over our personal life has detrimental effects. In one US survey:

- 60 percent of people suffered from job-related stress, anxiety, and depression.

- 12 percent of people worked more than 50 hours in a week.

- The majority expressed dissatisfaction with their jobs.

Yet we’ve little to show for all this hassle. Economic circumstances in the US mean people are earning less, saving less, and accumulating more debt. Here are the numbers:

- The majority of wage earners haven’t seen their pay increase more than 5.3 percent since 2000.

- Before the 1980s, people saved over 10 percent of their income. Today, most save 5 percent or less.

- Fewer earnings and savings has led to more debt—about $11,000 for every person in the US.

There are two reasons that we choose money over life: We don’t know how to leave jobs we don’t like, and we don’t know how much money is “enough” for our happiness.

We Don’t Know How to Leave Jobs We Don’t Like

We don’t know how to leave jobs we don’t like because our work is tied to our identity, and we think we need to stay with jobs to earn money.

Identity

We conflate our job with our identity and worth as human beings. We also judge others based on their work. For instance, teaching is considered less prestigious than being a doctor, even though guiding and instructing children is arguably just as demanding. This is called jobism.

We spend so much time working that it has become the main way that we express ourselves, but this wasn’t always the case. We used to develop identity from our interactions in the community, through places like churches and neighborhoods.

Additional Reasons

There are three additional reasons that we stay in jobs we don’t like:

1. We face burnout, boredom if the work isn’t challenging enough, and a competitive atmosphere that is hard to succeed in. Though these seem like reasons to leave a job, we often interpret these circumstances as the norm in all workplaces—and any notion we had of finding the dream job of our childhoods gets filed away as idealistic. We think that this is the best we can get.

Example: Elaine wished she could leave her job as a computer programmer. The work bored her and she hated it. But she worked well enough that she wouldn’t be fired. Her earnings bought luxuries, like a sports car, but not satisfaction. She thought that life would always be this way, no matter the work she did.

2. We have debts—house payments, student loans, and more—that can make leaving a job difficult.

3. We have bought into the idea that we need money and the things it can buy to satisfy our needs.

We Don’t Know How Much Money Is “Enough” for Our Happiness

The second reason we choose money over life is that we don’t recognize when we have “enough” money. This is due to money lessons we learned in childhood and continue to apply as adults.

Childhood: Learning About Money

Many habits get solidified in childhood before we’re fully aware of them. When we carry these behaviors into adulthood unchecked, they can be harmful to our wellbeing.

Young children are hard-wired to meet their needs externally. If you were hungry, you’d cry and a parent fed you. Over time, you learned that not only could your basic needs be met by looking outside of yourself, but so could your desire for niceties—things beyond basic needs that enriched your life in some way, like a bicycle or a toy. But you learned that you needed money for such goods—and to have money, you needed to work.

Eventually, you expanded from using money to purchase basic goods and niceties to purchasing luxury goods. As you got older, you continued to look externally to address your emotional needs. This required spending money.

Adulthood: The Elusiveness of Happiness

It’s difficult to discern when we have enough. As we enter adulthood, we expect to accumulate wealth and possessions as we move through our lives. From lavish weddings to ice cream cones, we spend money both to mark our successes and to comfort ourselves in times of distress or boredom.

We think that we’ll feel happier and more satisfied as we spend money. But often, this isn’t the case. Most people want about 50 percent more income than they have. A study asked people to state their income and rate their happiness on a scale of 1 to 5, from completely unhappy to completely fulfilled. Scores ranged from 2.6-2.8 regardless of how much money the person earned—people earning below $1,500 a month and over $6,000 a month gave roughly the same responses.

To remedy this, we need to identify what is enough for us, both from a money perspective and a stuff perspective. This means:

- Examining how much money it takes to satisfy basic needs, niceties, and even some luxuries.

- Spending within our means so that we don’t take on debt.

- Avoiding having excess stuff, or clutter, that causes us stress, guilt, or shame. When we accumulate stuff that we don’t use, like once-worn clothes that we then donate, we question our motives for buying them in the first place, augmenting our dissatisfaction.

- Reducing clutter. This includes spending time and money on immaterial experiences and activities that have no meaning for us, like going to a networking event that you have no interest in.

In Step 4, you’ll use several questions to examine your spending and determine what is enough for you.

Problem #2: Choosing Money Over Life Hurts the Earth

Not only is spending more money unlikely to make us happier, it also has severe consequences for the earth. Everything we consume comes from this planet, from the sand that’s used to make the glass in our windows to the cashmere in our sweaters. If everyone consumed resources at the rate of the US, we’d completely deplete the earth’s resources in less than a year.

Because the planet’s resources are finite, consuming more than our fair share means that we’re robbing resources from the generations to come.

A History of Consumption

Why do we consume so much? It started with the Industrial Revolution. Machines started making goods and fulfilling more of people’s needs. By the 1920s, people felt like they had enough—they worked enough, and got paid enough. They asked to reduce their working hours in order to relax.

But these changes didn’t sit well with two groups:

- Protestants valued a strong work ethic and eschewed leisure. They thought leisure opened the door to corruption by the devil and a pathway to other sins.

- Industrialists also balked at the idea of people working less. If people weren’t interested in buying goods and services, factories wouldn’t need to produce them at the same rate. This would halt economic growth, threatening civilization itself.

For production to continue at the same rate or faster—and to continue to line the pockets of industrialists—there needed to be new demand for factory-produced goods and services. Thus, marketing was born: the practice of convincing people to buy things they didn’t need.

Doing this required changing people’s ideas about why they worked. Advertising played a critical role, making a person feel that they lack something, then providing the solution to their problem—a product or service for purchase. Marketing taught people that:

- They should earn enough money to cover their basic needs and to buy things they want.

- Leisure no longer meant just relaxation—it became a time to fill with things and activities you buy to relax, like travel and entertainment.

Breaking the Consumption Habit

The first step toward breaking your consumption habit is dismantling the myths you hold about growth, technology, and climate change.

Myth #1: Growth Is Good

Our economy is still based on the idea that growth is good. We think growth will alleviate poverty, decrease unemployment, and improve the standard of living. Because not spending money could lead to these woes, we’ve become convinced that it’s not only our right to consume, but our patriotic duty. By this same rationale, saving money is seen as not being patriotic and not contributing to the economy.

But the “growth is good” mantra ignores that the planet has limited resources. Every plant and animal is limited by access to resources, like water. And nothing lives forever. If we harvest a species of fish too fast for the population to replenish, then we drive that species to extinction.

Breaking down the myth that more is better will help us break harmful consumption patterns that deplete the planet of its resources.

Myth #2: We Just Need the Right Technology or Policy

Sometimes we’re too quick to look to technology or government to solve the world’s problems. Here’s why:

- We think better technology will help. It has helped address pressing problems, like developing the polio vaccine, so it’s easy to think it’ll save us again.

- We think that our government will step in, creating programs to solve pressing issues.

- We blame third world countries for the world’s problems. We worry about overpopulation there, while doing little to address overconsumption in our own country.

Looking to technology and government makes us feel powerless to effect any change.

Myth #3: The Danger Isn’t So Immediate

Humans are hardwired to react to threats that pose immediate danger, like being hunted by a predator. We have trouble addressing less immediate issues, like climate change—we just don’t feel in danger. We may not feel the danger, but if we don’t act soon, our planet and future generations will pay.

Instead, we need to accept scientific understanding of the climate crisis and work to change our habits with the same urgency as if we were facing down a bear. Working through the steps in this book will help build sustainable consumption patterns that will preserve the planet for future generations.

Step 1: Visualize Earnings and Calculate Net Worth

The first step in examining your relationship with money is to systematically take an inventory of all the money you have earned and the material possessions you own.

Though you may feel tempted to skip this step, don’t. Examining the money that has come into your life can be a powerful step toward understanding not only your earning power, but how you choose to spend it. In later steps, you’ll analyze your spending to evaluate if it helps you satisfy your “enough.”

While completing this step, and all further steps, practice the following:

- Don’t shame or blame yourself for what you learn. Your earnings and net worth don’t equal your value as a person.

- Be thorough in attempting to dig up all that you can about your financial past and present. That way, you’ll get the clearest view of how much money you’ve earned.

Here are the steps:

1. Calculate how much money you’ve earned in your lifetime. Include income from your first babysitting job when you were 13 to your current job, and all the full-time jobs, side gigs, and gifts received in between.

To round up all sources of income, look at:

- Income tax returns

- W-2 forms

- Bank statements

- What the Social Security Administration says you’ve earned in your life so far

- Checkbook ledgers

- Money you received as a gift, or won

- Earnings from work that you might not have reported on your taxes, such as tips and babysitting wages

- Loans

- Capital gains records

- Illegal sources

Add in any earnings that you didn’t declare in tax returns, like tips you earned but didn’t report, and income from odd jobs. It may take a few days to comb through these records.

2. Calculate your net worth. Sort your possessions into things you own and things you owe—these are your assets and liabilities, respectively.

Liquid assets include cash itself and anything you can exchange for cash, including:

- Money in checking and savings accounts

- Savings bonds (US)

- Bonds

- Stocks

- Brokerage accounts

- Money Market accounts

- Mutual Funds

- Certificates of Deposit or other savings certificates

- Any cash you have on hand

- Security deposits

- Debts owed to you that you could collect

Fixed assets include any material possession you own worth a dollar or more. Assign a value for each of these possessions. Look at online marketplaces, such as auctions or Craigslist if you need help.

Write down liabilities as any debts you have or money you owe. If you list an asset like your car or house, make sure you list the money you owe on it as a liability.

To calculate your net worth, find the sum of your liquid and fixed assets. Then, subtract your liabilities.

Exercise: Determine the Flow of Money in Your Life

Complete the first step in Your Money or Your Life.

Make a list of all your income sources in your lifetime and how much you earned from each.

List all of your assets and liabilities. Then, subtract your liabilities from your assets to calculate your net worth.

What’s surprising or notable about your earnings? About your net worth?

You’ve now calculated your earning potential and your net worth. List some things you have to show for it (a house, jet ski, handbag, and so on).

Step 2: Tracking Your Money

To understand why you don’t have to choose between your money or your life, you need to understand what money is. It’s hard to define money, but it’s important—your personal definition may be preventing you from understanding how much you truly earn and how many hours you spend on work and work-related activities. After we define money, we’ll define what it means to be financially independent.

Lastly, we’ll cover Step 2 of the program. You’ll learn to:

- Calculate your real hourly wage

- Track your expenses

What Is Money, Really?

There are 4 basic ways people think about money:

- It’s a material—literally the bills, plastic, or transaction that allows for the purchasing of goods.

- It’s a reflection of our psychology, embodying our dreams and fears. How you spend money can reflect your personality, whether you’re a penny-pincher or like to spend liberally.

- It’s a reflection of our culture: thinking that “more is better” and that we have a role in growing the economy.

- It’s “life energy”—we are willing to dedicate our time and energy in exchange for money. This is the most useful definition of money because it’s consistent in most situations.

Defining money as life energy allows us to make statements like, “I invested 8 hours of my life to pay for this pair of shoes”—we can see exactly how much time and energy goes into each purchase.

Your life has a finite number of hours. In general, you can assume that half of the hours remaining in your life will be filled with doing basic body-related things: sleeping, eating, exercising, and more. That leaves the other half to squeeze in work and everything else that matters to you, like spending time with family.

Escaping the Money Game

Like it or not, we are all part of the money game—the buying and selling of goods and services. We need some to survive, but advertisements encourage us to consume things beyond the basic necessities. For example, you might be convinced to upgrade your phone even when you have a functional one.

In addition, there are some economic indicators that force us to keep playing:

- Inflation

- Cost of living

- Recession and depression

We’ve been trained to be sensitive to these kinds of economic indicators. If we’re told something is off, we respond accordingly. Here are some examples:

- If we hear that a recession is imminent, we might decide to forgo taking a vacation that year, despite having a stable job and plenty of savings.

- If the news says that the cost of living in our area has increased, it makes us feel poorer, playing off of our existing concerns about money. However, the consumer price index, which is used to evaluate cost of living, continues to add items that were once considered luxuries, like cell phones. We’re expected to need more things, even if our earnings haven’t risen to match.

The money game’s ability to keep us spending isn’t unlike the premise of the popular film, The Matrix . In the movie, machines pacify humans through a simulated reality and use human energy to power themselves. The main character, Neo, is offered a “red pill” to be able to see this reality.

Understanding that money is life energy is like taking the red pill. You learn to:

- Identify what you need, rather than being convinced to squander your money or time.

- Reflect on your spending, and decide if you would spend differently in the future.

You can’t decide whether or not to play the game, but you can make more cognizant decisions about when to play. In some instances, you might realize that spending money isn’t the best way to satisfy your needs or the needs of others. Instead, you can make use of other resources at your disposal, such as affection or expertise.

Financial Independence: Myth and Reality

Just as you need to understand the definition of “money” to improve your relationship with it, you need to understand what financial independence is in order to work toward it.

When you hear the term, “financial independence,” you may think of becoming rich and the myriad of luxuries that would afford, like endless, swanky vacations. But being “rich” is a relative term— you can’t feel rich unless other people have less . Striving to become rich isn’t a realistic goal and plays into the “more is better” myth.

Financial Independence means having the money you need to survive, plus more for the things you deem important for your life. This is the definition of “enough.” It will be different from person to person.

Aside from learning what your “enough” looks like, achieving Financial Independence means:

- Spending money based on your choices, not at the whims of your circumstances.

- Interrupting your assumptions about how you should or shouldn’t think about money.

- Understanding your finances so that you feel confident.

- Acknowledging the emotions you experience when thinking about money—anger, guilt—and moving beyond to make choices that fit your values.

Step 2: Track Your Money

Step 2 has two parts. First, you’ll calculate your real hourly wage. Then, you’ll start tracking every penny you spend.

Step 2.1: Calculate Your Real Hourly Wage

Calculating your real hourly wage is an important step in understanding your relationship with money. Most people take their hourly wage at face value (“I earn $25 per hour”). This neglects two things:

- The time they spend doing work-related activities.

- The money they spend on work-related expenses.

A real hourly wage accounts for all of these factors. Ultimately, you’ll determine how much money your “life energy” is currently worth.

For some categories, like commuting, the time and cost will be obvious and built-in. For others, you need to assign a value.

1. Create a table to calculate your real wage, as shown in this example:

| Hours/Week | Dollars/Week | Dollars/Hour | |

| Job (before adjustments) | 40 | 1,000 | 25 |

| Adjustments | |||

| Wardrobe/Upkeep | +1.5 | -25 | |

| Commuting | +10 | -125 | |

| Food | +8 | -80 | |

| Sickness from work stress | +1 | -25 | |

| Escapism | +5.5 | -45 | |

| Unwinding | +5 | -30 | |

| Time Off | +5 | -30 | |

| Total Adjustments (time and money spent maintaining job) | +36 | -360 | |

| Actual Total (job with adjustments) | 76 | -640 | 8.42 |

2. Fill in the second row with the hours/week you work, dollars/week you receive, and your hourly wage.

3. Below, record the number of hours you spend on work and work-related activities and assign a cost. Here are the basic categories and some examples; feel free to add your own:

- Wardrobe and upkeep of your physical appearance: time spent grooming yourself for work each day, such as getting dressed and putting on makeup, as well as time and money spent on shopping for professional clothing, shaving your legs, etc.

- Commuting: time spent commuting to and from work, and the associated costs, like gas and insurance.

- Food: the cost of any beverage or meal that you eat out because of work, from coffee to any dining out you do because your job leaves little time to cook.

- Sickness from work stress: any time that you get sick due to stress from your job.

- Escapism: activities that you treat yourself to as compensation for how stressful your job is, like binge-watching The Great British Baking Show to take your mind off of work after a stressful meeting.

- Unwinding: time spent destressing from your job, like talking about it, or money spent on recreational substances.

- Time off: any vacation that you consider necessary to keep you coming back to work. It’ll likely be the vacation where you’re not doing much—maybe just parking yourself on the beach to recharge for a week.

- Miscellaneous: anything else you spend time or money on for your job, like taking out your frustration with your job onto your partner, or buying tools.

4. Add up all of the hours and money in columns 2 and 3 to calculate the hours you dedicate to work and work-related activities, and how much you spend on work per week.

5. Divide your adjusted dollars/week by your adjusted hours/week to find your real hourly wage.

In the above example, a job where the person’s hourly rate is $25 an hour really only pays $8.42 an hour when factoring in all of the time and money spent on job-related activity.

Use this real hourly wage to evaluate whether your job, and future jobs, are worth your time. For example, if a job in the city pays more than a job close by, but you have to spend time and money commuting, it may be less lucrative over time than something close by that pays less.

Optional Step

You can also calculate the value of your time down to the minute, which allows you to decide if a purchase is worth your time. In the example above, the person must work 7.12 minutes for each dollar spent. Let’s say they want to buy a new set of earphones for $40. That would require nearly 285 minutes of work time. Is it worth it?

Step 2.2: Track Money, Down to the Penny, You Receive and Spend

Tracking the money that comes into and goes out of your life allows you to reclaim control over your spending. You can begin to discern necessary and fulfilling purchases from frivolous ones. You make a habit of taking an honest look at how much you earn and what you spend it on, leaving no room for exasperation, excuses, or resignation.

People who are in control of their finances know exactly how much money they spend, and on what. Consider it a solid investment in your financial future.

Start by tracking every penny. There are many formats to do this. You can use physical or digital formats, such as pocket-sized notebooks, calendars, notes on your phone or computer, or online software that tracks spending from your bank accounts.

Ideally, break down payments where you bought more than one thing into each individual item. For example, when you buy groceries, record each individual item. Use round numbers for most items as long as the total accounts for the cents involved.

It’s easy to get wishy-washy or want to round to the nearest dollar. But for starters, in service of getting the most accurate picture possible of your financial life, aim for the nearest penny. If you eventually round to bigger coins, or even whole dollars, that is fine.

Exercise: Question Your Money Assumptions

Examine advice you’ve received about money.

Think of a message, lesson, or piece of advice you got from your parents about money as a kid. What did you think of it at the time?

Do you apply this lesson to your financial life now? If so, in what way? If not, why not?

Knowing that money is your life energy, would you modify how you apply your parents’ advice in any way? If so, how?

Step 3: Creating a Monthly Tabulation

In this chapter, you’ll take the data you have recorded about your spending and create a monthly tabulation.

First, you will develop different spending categories for what you spend money on. Next, you will create a way of tabulating your monthly spending and sort your expenses for the month into each of your categories. Lastly, you’ll use your real hourly wage to calculate how much life energy you spent in each category.

How Is This Different From a Budget?

Some finance programs have you make a budget to help you plan how to spend your money.

This program avoids two pitfalls of budgets:

- They aren’t detailed enough to capture your unique spending habits. Developing your own spending categories will help you get a more accurate picture of your spending patterns.

- They don’t encourage you to reflect on your spending. With a monthly tabulation, you’ll gain a clearer picture of your spending and evaluate whether or not it’s worth it.

Step 3: Categorize Monthly Expenses

Step 3.1 Develop Your Categories and Subcategories

First, develop spending categories and subcategories that capture what you spend money on each month. For example, let’s say one of your spending categories is “Food.” If you realize that you’re frequently buying vending machine snacks in your office building, include “vending machine snacks” as a subcategory of “Food.” Find a balance between capturing more detail than the broad category, but not driving yourself crazy.

Here are some potential categories and subcategories:

Food

- Food for home eating

- Food for sharing with guests

- Restaurant visits

- Snacks

Housing

- Rent or Mortgage

- Utilities

- Renter’s insurance

Clothing

- Leisure

- Work

- Athletic

- Shoes

Pro-tip: consider subcategories that reflect emotional reasons for spending, like buying clothes to make yourself feel better.

Transportation

- Car

- Public Transit

- Ride Shares

- Auto Insurance

Electronics and Tech

- Cell phone

- Internet

- Wearables (ie. a smartwatch)

For Fun

- Television/Movie streaming services

- Music streaming services

- News subscriptions

- Alcohol from bars

- Movies

- Kids’ entertainment

Health

- Gym Membership

- Vitamins

- Prescription drugs

- Nonprescription drugs

- Health Insurance

- Doctor’s visits

Unexpected Expenses

There are often large, unexpected expenses that occur each month. Examples include:

- Car repair payments

- Once-a-year insurance expenses

- Paying down a chunk of your house

Not all unexpected expenses come up each month, but usually one will. Choose a strategy to account for these. You have two options:

- Put unexpected expenses in whichever subcategory they fall in. Over time, you’ll build a sense of how much you spend on unexpected expenses each month, regardless of category, and learn to have money on hand to deal with them.

- Prorate expenses that you pay once per year across 12 months. If you pay $600 for homeowners insurance once a year, divide that by twelve and include the monthly figure in your expenses each month.

Miscellaneous Categories and Considerations

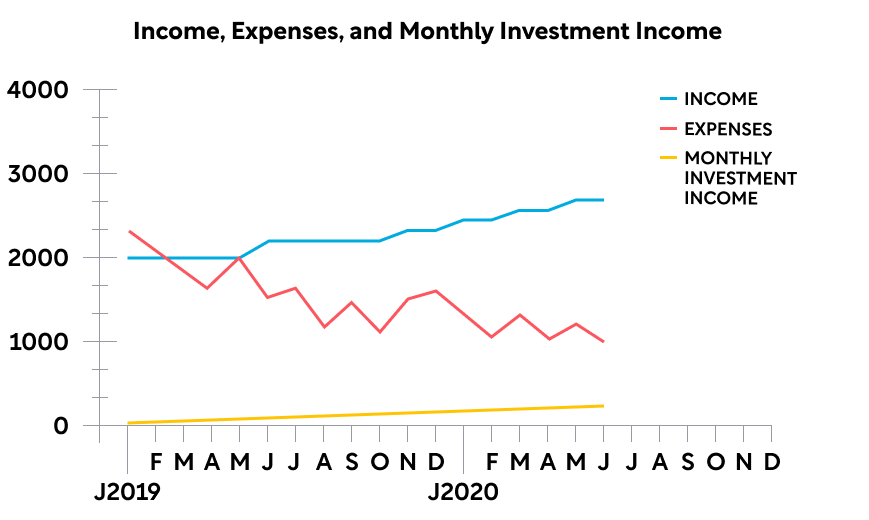

In addition to the above, make a small table that includes each of your income streams. Eventually, this will include interest from Investment Income (discussed in Chapters 8 and 9)

Also make sure that you separate business and personal expenses. For example, what percentage of your time using your phone goes toward work versus personal use? Split the cost accordingly.

Step 3.2: Create Your Tabulation System

List the categories you’ve created in a spreadsheet or similar tool. You’ll use this to sort your monthly expenses into your categories and subcategories.

The table below shows one way to set it up:

| Expenses | Total Dollars | Life Energy | 1. | 2. | 3. |

| Clothing | |||||

| Leisure | |||||

| Work | |||||

| Athletic | |||||

| Shoes | |||||

| For Fun | |||||

| Streaming services | |||||

| News Subscriptions | |||||

| Movies | |||||

| etc. |

| Income | |

| Loans | |

| Tips and/or Bonuses | |

| Interest | |

| Paychecks |

(1) Total spent __ (2) Total income __

(2)-(1) Savings __

Don’t worry about the blank columns for now. You’ll use them in Step 4.

Once your system is in place, follow these steps to understand your spending for the month:

- Place each transaction in its appropriate subcategory.

- Total the transactions in each subcategory, category, and overall.

- Count any cash you have leftover, and note the balance of your bank accounts.

- Calculate your savings for the month:

- (Income- Total Expenses) +/- error

- Error is any unaccounted for money you have, lost or gained.

- For each subcategory, calculate the hours of life energy you spent by dividing the total by your real hourly wage.

- Example: $80 on magazines divided by $8.42 = 9.5 hours of life energy

- Assess: are the hours of life energy that you expended to make that purchase worth it?

Exercise: Assess Your Spending

Reflect on your spending in the past month.

What categories did you spend the most life energy on?

Which categories did you spend a surprising amount on, either less or more than you expected?

Which subcategories did you spend the most life energy on?

Which subcategories did you spend a surprising amount on, either less or more than you expected?

If you’ve budgeted in the past, how has this experience been different?

Step 4: Aligning Spending With Values, Purpose, and Dreams

The next step in understanding how you spend your life’s energy is to look at the things—material and immaterial—that you want in life. First, you have to get in touch with what you are trying to achieve in life—your values, purpose, and dreams. We’ll explore some questions to help you define each of these things for yourself.

Once you’ve identified the above, you’ll use it as a guide for Step 4—looking at your monthly tabulation and asking a series of questions to assess whether your spending aligns with your values, purpose, and dreams.

Values, Purpose, and Dreams

Values

Your values reflect your beliefs. We feel content when our behavior is consistent with our values. But how we choose to spend our time and life energy doesn’t always reflect our true values. Sometimes we need to adjust how we spend our time and/or money.

For example, maybe you value reducing your carbon emissions to combat global warming. You’d like to express that value by commuting by bike, but instead, you justify driving your car to work most days because the bike commute adds an extra 20 minutes of travel. To solve this, you elect to prep your lunch and work bag at night to reclaim 20 minutes of your morning, allowing you to bike.

You’ll explore aligning your spending with your values later in this chapter.

Purpose

Similarly to values, identifying your life’s purpose can guide your spending habits and how you use your time.

There are two kinds of purpose:

- Your general purpose is more short-term and personal. It’s when you act or do something in the present that allows you to achieve something important later. For example, you save money now so that you can take a sustainable farming course later.

- Life purpose is more long-term and focused on the bigger picture—how you choose to put your life energy to use to contribute to the world. It’s recognizing that you are a small part of a bigger whole, but instead of feeling insignificant, you’re empowered to contribute your talents to important causes.

If our purpose in life is out of focus, we amble along with little direction. Identifying your purpose allows you to align your life’s energy with it.

Finding Your Life’s Purpose

Ecologist and writer Joanna Macy suggests three approaches for finding your life’s purpose:

- Identify your passion. Think about a cause or activity that you’d dedicate yourself to, not to escape or avoid your life, but because you care about it. Maybe you’re a skilled kayaker and you decide to lead guided kayaking tours of your favorite local lake.

- Identify your pain. If you’ve navigated a tough experience, you may have expertise to help others in similar situations. For example, if a close friend of yours committed suicide, you could dedicate part of your time to suicide prevention organizations.

- Identify problems close by. There may be problems in your community that you feel called to make better. For example, you start writing regular letters to get your city council to allocate money to homeless services.

Rediscovering Your Dreams

Another way to get in touch with your sense of purpose is to revisit childhood dreams. These dreams can indicate how we’d enjoy spending our time.

But sometimes, we abandon our dreams. There are two main reasons:

- We dismiss dreams as too childish, thinking they will never come true. Trying to get your painting career off the ground might be difficult if your current desk job takes up all of your time, and you have bills to pay. More often than not, you might just stick with work you don’t like, as discussed in Step 1.

- We take on debt, and dreams start to feel impossible. Sometimes achieving a dream involves going into debt, as in getting a college education. This debt limits our ability to achieve additional dreams—we can’t afford to pursue them.

To find fulfillment, we have to reclaim our dreams and take steps to achieving them while dealing with our other obligations, like debts or bills.

At first, it might feel difficult to access and work toward dreams that you’ve set aside for so long. Answer the questions below to remember your dreams:

- When you were a kid, what did you picture yourself doing for work?

- What is something you’ve done—in your career, or in general—that you’re proud of?

- What is something that you’ve wanted to do for a long time, but haven’t yet?

- What makes you feel fulfilled? How does it relate to money?

- You learn you have one year, max, left to live. What would you choose to do with that time?

- If you could live without having to work for money, how would you spend your time?

Step 4: Evaluate Monthly Spending

Now that you have a sense of your values, purpose, and dreams, you’ll use them as benchmarks to evaluate your spending in each of your categories and subcategories.

Using the 3 blank columns on your monthly tabulation, ask yourself the following questions for each category and subcategory:

Question 1: Is the Amount of Happiness and Contentment I Got From These Purchases Worth the Life Energy I Spent?

Ideally, the more money you spend, the more enjoyment you should get. But it’s common to spend money that doesn’t bring adequate fulfillment for the expense. Question 1 helps identify areas where you’re overspending relative to your enjoyment. On the flip side, it helps you see spending categories that bring great joy to your life that you could spend more money on. You’ll start to map the intersection between spending and fulfillment—what’s enough for you.

Look at each subcategory and category of your spreadsheet, and assign one of three symbols in the first column for each:

- Use a “-” sign if you didn’t get fulfillment proportional to what you spent and should spend less.

- Use a “+” sign if you got fulfillment proportional to what you spent and think you should spend more.

- Use a “0” if you got fulfillment proportional to what you spent and think your spending should stay the same.

- For example, you ask Question 1 looking at the $50 you spent on magazine subscriptions in the past month and realize that most of those magazines regularly go unread. Because you don’t enjoy them in proportion to their cost, you mark a “-” in the first column, indicating that you can spend less.

Do this as objectively as you can without thinking too hard about the amount you spent. This will help you evaluate the subcategory purely from an enjoyment perspective without passing judgment.

Asking monthly whether your spending brought you fulfillment will calibrate you to your “enough”—the intersection of your spending with fulfillment. Learning what your “enough” is rather than relying on external sources for fulfillment is a major component of making sure your spending leads to happiness.

Question 2: Is Spending This Amount of Life Energy Consistent With My Values and Purpose?

Next, you’ll examine your spending in each subcategory and category through the lens of your values and purpose.

Look at the next blank column, to the right of the column you used for Question 1. In this column, follow the same procedure as before, using “-”, “+”, and “0” to show when spending less money, more money, or the same amount is necessary to bring each particular category and subcategory in line with your values and life purpose.

For example, you spent about $25 dollars each week on lunches from chain restaurants and $16 on lunches from locally-owned businesses. You’re comfortable with the total amount spent, but you’d prefer that the majority of the lunch money go to locally-owned businesses because you value keeping wealth in the local community. To reflect this, you mark a “-” for the chain restaurants subcategory, and a “+” for the local businesses subcategory.

Question 3: If I Didn’t Have to Work for Money, Would I Spend More, Less, or the Same Amount of Life Energy?

Earlier in this chapter, you were asked to consider how you might spend your time if you didn’t have to work for money. Question 3 goes one step further, asking you to consider how you would spend your life energy (money) differently if you didn’t have to work for money.

Working often requires that we spend money on things like commuting. Asking Question 3 for each subcategory and category illuminates how much of your spending is due to work and work-related activities.

You may find that life would be cheaper if you didn’t have to work. For example, maybe you’d stop spending money on your fancy work wardrobe. But you might spend more in certain categories, like travel.

There are no right or wrong answers. The point is to imagine how your spending would look different under a different set of circumstances. Since you’re working toward financial independence—not having to work for money—this will ultimately help you plan for life once you’re financially independent.

In the next blank column, to the right of the column you used for Question 2, follow the same procedure as before, marking a “-”, “+”, and “0” to show how you think your expenses in each of these categories would change.

Spotting Patterns and Making Adjustments

Once you’ve gone through each question with each of your subcategories and categories, the next step is to return to each subcategory to reflect.

Evaluating your subcategories according to each question may make clear the areas to adjust. For example, if you marked a minus indicating that you didn’t derive enough enjoyment from what you spent on movies, and you marked a minus indicating it didn’t align with your values and purpose, this is a sign you should adjust your spending in that category.

Again, try to do this as objectively as possible, and go easy on yourself. Ultimately, the goal is to adjust your spending so that you only have 0s (“I’m spending exactly what I want to spend in this category”) or pluses (“Spending life energy in this category brings me great fulfillment in proportion to what I spend, and spending even more will bring me even greater happiness.”)

This process allows you to redirect or eliminate excess spending and get closer to your “enough.”

(Optional) Question 4: In a World Where Everyone Could Meet Their Basic Needs and Had Enough, How Would My Spending in This Category Change?

We over-consume material goods. If everyone in the world did this, we’d quickly deplete the earth’s resources. To interrupt this tendency, consider asking this fourth question to determine whether spending in each of your subcategories aligns with people around the world having enough to meet their needs now, and in the future.

Tailor this question to make it compelling to you. Here are 4 examples of ways to rephrase it:

- If everyone spent like this, would the world be a better place?

- Is this good for the environment/Earth/others?

- What would Jesus do?

- If everyone in the world were this mindful about how they spent their life energy, would it change the world?

Though this question isn’t required, you may find yourself naturally asking it after the first three.

Exercise: (Re)Discover Your Dreams

Explore your dreams, past and present.

When you were a kid, what did you picture yourself doing for work? Why?

How did this image of your future work change as you got older? Why?

How closely does what you do for work reflect your dreams?

If you could live without having to work for money, what work would you choose? How would this better reflect your current dreams?

Step 5: Graphing Your Income

After completing the first four steps, you’re ready to do Step 5—visualizing your expenses and income on a hand-drawn or digital chart. Your graph will offer a clear representation of your finances over time, providing motivation to reduce your spending, pay down your debt, and build your savings.

First, we’ll tackle how to find motivation to continue with the program at this point. Then, we’ll outline how to complete Step 5, followed by a discussion of the benefits it will afford you over time—including reaching financial independence.

How to Keep Going

At this point, you may find it tempting to stop following the program. Perhaps you feel the first steps have only confirmed what you already knew, that you’re deeply in debt or spend money on things that don’t make you feel fulfilled.

If you follow the steps of this program, you’ll eventually reach financial independence. But it requires persistently working through the steps, and developing this habit takes time.

Here are three tips to keep moving forward:

- Consistently do the steps. Don’t consider them optional—work on them even if you don’t feel motivated to do so. Over time, it will start to feel less like a chore and more like a part of everyday life, just like taking a shower.

- Hold yourself accountable by sharing your progress with someone else. Just like exercising with a buddy, regularly discussing your experience with another person motivates you to do the work and improve. This could take many forms, from weekly check-ins to giving someone access to your online expense tracking tool.

- Create a graph to be able to track your monthly income and expenses. This is Step 5!

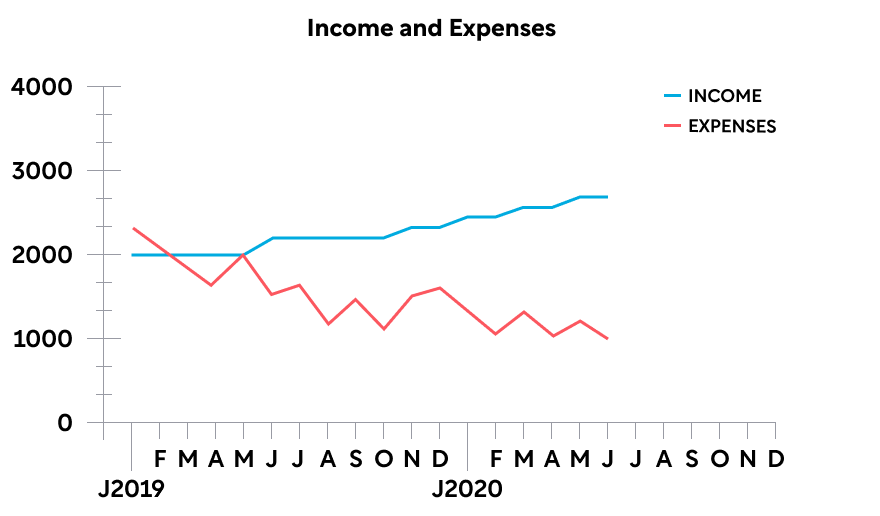

Step 5: Graph Your Income and Expenses

Charting your income, expenses, and savings over time will help you visualize your path to financial independence and stay motivated.

Decide if you want to make a paper chart or a digital one. Though programs like Microsoft Excel offer nice charts, a paper one is useful because you can hang it somewhere you will see it—and feel inspired by it—every day. Seeing it each day reminds you of why you’re following the steps—to spend less than you earn, climb out of debt, and increase your savings.

If you go with paper, get a sheet of graph paper that can accommodate up to 10 years of data. Choose an 18 by 12-inch piece of lined graph paper, or 36 by 24-inches. (If you can’t find graph paper, you can line a large blank sheet of paper yourself.)

Setting Up Your Graph

- On the horizontal, or x-axis, mark out time in months. Allow room for 5-10 years (60-120 months).

- On the vertical, or y-axis, mark out dollars. Start with 0, and allow enough room for your income to double, even if that feels impossible at the moment. Create a scale that causes your larger figure for this month—income or expenses—to be recorded halfway up the axis. For example, if your income this month is $3,500 and your expenses are $3,200, make the $3,500 mark of your vertical axis fall about in the middle.

- Each month, mark your monthly income and expenses. It’s helpful to use two different colors: one for monthly income, and one for monthly expenses. Draw a line from the current month to the previous month. Over time, your chart will look something like this:

The Benefits of Step 5

Completing this step each month offers several concrete benefits that will put you on the path to financial independence:

- You’ll strive to earn more than you spend.

- You’ll pay off your debts.

- You’ll build savings.

1. Earn More Than You Spend

The graph serves as a potent visual reminder of what you’re working toward—making the gap between your income and spending larger. This is your savings. By following each of the steps in this program, you can expect to lower your expenses by about 20 percent.

But take caution—after doing Step 4, you may be tempted to severely restrict your spending in certain categories. Though this will decrease your spending, it often isn’t sustainable in the long-term. For example, if you’re eating only beans and rice in an attempt to save money, you’ll likely see a decrease in your spending. But this is very restrictive, and you may feel like you don’t have enough variety in your diet to do it long-term. After one month, once you confirm that you can restrict your food spending, you may ease the restrictions, returning your food costs to what they used to be.

Rather than taking on severe restrictions you won’t be able to maintain in the long-term, simply ask the questions from Step 4, expand your chart through Step 5, and choose some strategies to reduce your spending in Step 6. This will naturally orient you toward spending within your means.

2. Pay off Your Debts

In order to become financially independent, you need to pay off your debt. When you no longer have debt to pay, those dollars are freed up for you to use elsewhere.

If you don’t proactively pay down your debt—paying more than you owe—you lower your income, and by extension, your savings, over time. For example, if you pay exactly what you owe on your thirty-year mortgage, you can end up paying 2-3 times the sales price of the house due to accumulating interest.

Your graph can motivate you to find creative ways to pay off debt faster and dissuade you from taking on more. For example, some people choose to forgo using credit cards altogether in order to avoid going further into debt and to encourage themselves to spend less money. Others have decided to take on a housemate to help pay down their mortgage faster.

3. Build Savings

Many people in the US are financially insecure and have little to no savings. A 2015 study found that 47 percent of people in the US would struggle to pay an unexpected $400 payment.

But the faster you save money, the more quickly you’ll reach financial independence. Once you pay off your debts, it becomes even easier to save money because you can save what you used to pay toward debt. Then, you can devise ways to boost your savings, such as cutting back on spending or adding income.

Over time, as you live within your means, work to pay off your debts, and increase your income (more on this in Steps 7-9), the space on your graph that represents savings will grow.

Step 6, Part 1: Strategies to Cut Spending

In this chapter, you’ll learn strategies to spend less. To better understand these strategies, we’ll first explore what it means to be frugal. This will help you reframe your thinking around spending money and learn to meet your needs in creative ways.

The True Meaning of Frugality

A key component of this program is finding fulfillment by spending your life energy—money—on what brings you happiness and learning to live with what is “enough” for you. Learning to practice frugality will help you do this.

While most people think that frugality means severely restricting your spending, it’s really about enjoying or making use of something—and you don’t have to own things to enjoy them. Yet people often try to satisfy their desires by buying things. Sometimes we like buying things because of the symbolism of owning them and the approval we get from others. For example, owning a fancy car is symbolic of a successful career. But practicing frugality means being able to enjoy stuff for what it gives you materially, not what it symbolizes to you.

To practice frugality, cultivate a higher joy-to-things ratio. If you enjoy getting things more than having and using things, this could be a sign that you need to improve your joy-to-things ratio. For example, if you have 5 perfectly good pairs of shoes but aren’t excited about wearing any of them, you might derive more enjoyment from getting things than using them. In contrast, if you enjoy wearing all the shoes you own, you buy only what you need and enjoy it to its fullest.

Ideally, take joy in each thing you use. This will help you avoid running toward the next material thing in search of fulfillment.

Step 6, Part 1: Strategies to Cut Spending

There are 9 general strategies to help you cut how much you spend. In Step 6, Part 2, we’ll look at 11 categories to cut spending from.

1. Avoid Shopping

As we’ve discussed, we’ve been conditioned to fill immaterial needs with material goods. Thus, when we shop, we feel tempted to buy things, even if we didn’t plan to spend money in the first place.

Here’s how you can shop less:

- Don’t go shopping when you don’t have anything you plan to buy. Be deliberate with your purchases.

- Don’t mindlessly scroll through shopping websites for amusement. Only visit these when doing research or when you have a plan for what to buy.

- Handle promotional emails by unsubscribing or filtering them. Emails can trigger shopping desires.

- If you have an itch to buy something, wait a few days so you can figure out if you really need it or whether you’re just impulse buying. Research shows impulse buying is common (75% of people admit doing it), but the majority who do it regret it later.

- Pay attention to your shopping triggers. Men tend to impulse buy when drunk; women do it when they’re sad or bored.

2. Spend Only What You Can Comfortably Afford

Try to limit spending to things you can afford without having to take on additional debt. Here are some general strategies:

- If you use credit cards, spend only what you can pay off each month.

- If you want to buy something, but don’t have enough money, wait to buy until you do.

But what about buying houses, where most people have to take on debt? Investing in housing or something else that appreciates in value over time, can be a good investment. Always make sure to weigh your choices to take on as little debt as possible, and work to pay it off quickly.

3. Repair Your Possessions

Every time we buy something new, there are energy, labor, and environmental costs that go into producing that item. Though it may be tempting to buy cheap replacements for things that break, you’ll save resources and maybe even money in the long-run by repairing things instead of replacing them with new ones.

4. Use Stuff to the End

Many perfectly good items end up in the landfill just because we decide we want a newer item instead. Using something until it’s completely worn out helps you avoid frequent spending on the same items.

Here are some more strategies to use things longer:

- If you do successfully wear things out for their intended purpose, ask whether you can repurpose them in some way. For example, use grubby dish towels as cleaning rags instead. Look to the internet for suggestions.

- Resolve to upgrade less often than you usually do. For example, instead of buying the latest phone model every year, resolve to only upgrade every two years.

If you’re already on the frugal side, remember not to hold onto items so long that it costs you more life energy than it’s worth. For example, if you’ve worn your running shoes so thin that they’re hurting your knees, invest in new shoes—they’ll be cheaper than having to pay for knee surgery.

5. Dive Into DIY

These days there are more resources available than ever to help you learn how to do work yourself. Take advantage of online classes and YouTube videos dedicated to imparting new skills. If you do choose to hire out the work, watch it being done and use it as an opportunity to learn something that you can use later.

6. Think About What You Need

Thinking about what you need ahead of time can be a powerful tool to avoid buying things on a whim.

Here are some strategies to plan for long-term purchases:

- Create a list of things you anticipate needing to buy in the coming year.

- Research different brands and the price range of the item.

- Use sites such as online sellers or Craigslist to compare pricing, and set notifications to learn when an item has dropped in price.

- Buy around the holidays, or other times when retailers offer discounts.

Anticipate things you’ll need in the short-term, too. For example, rather than buying expensive one-off items at a convenience store, think about what you need before you need it and try to buy it ahead during a supermarket trip or online where you can get it for cheaper.

7. Investigate Durability and Multipurpose Uses

In addition to price research, investigate how long something will last. If you plan to use something frequently, learn if it will last enough time to make it worth its price. On the other hand, if you don’t plan to use a product that frequently, you don’t need to invest as much money in ensuring it’s durably constructed. Less frequent use means it’ll naturally last longer.

Here are two ways to assess a product’s durability:

- Examine it in-person. Look for signs like well-sewn seams and strong material.

- Read online reviews where users share their impressions and experiences.

For example, let’s say you’re in the market for a washing machine. You come across a model that seems like a reasonable price, but notice that most of the online reviewers have checked a box saying they would not recommend buying it. Plus, many complain that the machine broke down after just a few uses and required frequent repairs, costing them more money in the long-run. You decide it’s worth looking into a slightly more expensive machine that users recommend.

Buying multipurpose items also saves you money because you pay the price of one item instead of several. For example, one all-purpose pot can eliminate the need for other appliances like a rice cooker or deep fryer.

8. Don’t Pay Full Price

There are 4 main ways to purchase items for less than their original price:

- Search for the best price. Use price-comparison tools on your web browser or metasearch sites to find which retailers have the best prices. Call retailers that don’t list their prices online. Many retailers have programs to match lower prices from other stores in town, or even some online stores.

- Learn to haggle. An item’s listing price is usually high. There’s no harm in asking for a lower price. Ask for a lower price when a sale has already ended, when you’re paying in cash, or for items already being offered at a discount. This strategy works best at small, locally-owned stores.

- Buy previously owned or used items. Many items put up for sale are still in very good condition. Try thrift stores, garage sales, and online sites like eBay and Craigslist. Garage sales tend to be best for small home appliances and furniture, while thrift stores are best for clothes. But thrift stores often offer more than clothes, so explore widely.

- Get stuff for free. Sites like Buy Nothing Project and FreeCycle Network connect people with goods others are giving away.

9. Devise New Ways to Meet Your Needs

Once again, living frugally is not about living a life of deprivation. It’s about learning to meet your needs without having to spend vast sums of money, and ideally, without spending much money at all. In order to do this, we need to listen to our needs and desires and ask if they can be met without spending money.

For example, we might value freedom and look to travel to satisfy it. Travel allows us to feel free in our movement. But perhaps the desire to travel is really a desire for novel experiences and a break from our routines. In that case, it might be possible to satisfy that need closer to home by seeking out novel experiences in our own area. We could take a vacation within a few hours drive of where we live, or explore a new part of town we’ve never been to before.

Step 6, Part 2: Categories to Cut Spending

Now that you have some general strategies for how to limit spending, we’ll look at some specific suggestions for cutting expenses across 11 categories.

1. Banking and Loans

Many big-name banks have high fees associated with opening and maintaining accounts with them. Instead, open accounts with a credit union. Credit unions are not-for-profit, which translates to having lower fees and better interest rates than for-profit banks.

In general, most banks, credit union or not, will charge you a fee if you attempt to spend more money than you have, known as overdrawing. Avoid this by using your bank’s online tools and other money management software to track what you spend, set up automatic bill pay, and alert you when an account balance is low.

2. Housing

Popular wisdom of the past century says to aim to spend about 25 percent of your monthly income on housing. But these days, people often spend 40 percent or more of their income on housing.

Cut your housing costs with these strategies:

- Join cooperative housing. Co-op living allows you to have your own space while sharing common responsibilities like cooking and cleaning. They’re a great way to save money and grow your social circle.

- Move to an area of town where rent is less expensive, if possible.

- Move to a town that is less expensive if your job allows you to work from home.

- Choose smaller apartments or houses, which are cheaper to heat and cool.

- If you are looking to buy a home, consider buying a duplex or something that you can rent part of. This will allow you to lower your mortgage payment each month, and could even help you pay off your mortgage sooner.

3. Transportation

Owning a car is second only to buying a house in expensiveness. Apart from the initial cost, the maintenance, upkeep, and insurance add up. Avoiding car ownership entirely is often the cheapest way to go, with alternatives like car-sharing programs, renting cars, and public transportation abounding in cities.

If you still want or need to own a car, try to prioritize the following:

- Fuel efficiency. It’ll save you gas money in the long run.

- Reliability. It’ll save you maintenance and repair costs.

Even if you have a car with these qualities, you should still try to drive as little as possible to avoid costs associated with fuel and wear. Here are two suggestions:

- Minimize your commute to work by living closer, or work from home some days.

- Opt for walking, biking, and taking the bus.

4. Health Care

Saving money on health care tends to fall into three categories:

- Self-care

- Health Insurance

- Health Care